Balbharti Maharashtra State Board 12th Commerce Book Keeping & Accountancy Solutions Chapter 7 Bills of Exchange Textbook Exercise Questions and Answers.

Maharashtra State Board 12th Book Keeping & Accountancy Solutions Chapter 7 Bills of Exchange

Objective Questions

A. Select the correct option and rewrite the sentence:

Question 1.

The person on whom a bill is drawn is called a ______________

(a) Drawee

(b) Payee

(c) Drawer

(d) Acceptor

Answer:

(a) Drawee

Question 2.

Before acceptance the bill is called a ______________

(a) Order

(b) Request

(c) Draft

(d) Instrument

Answer:

(c) Draft

![]()

Question 3.

When the due date of the bill drawn falls due on a public holiday, the payment must be made on the ______________ day.

(a) same

(b) preceding

(c) next

(d) any

Answer:

(b) preceding

Question 4.

The due date of the bill drawn for 2 months on 23rd Nov. 2019 will be ______________

(a) 23rd Jan. 2020

(b) 25th Jan. 2019

(c) 26th Jan. 2019

(d) 25th Jan. 2020

Answer:

(d) 25th Jan. 2020

Question 5.

Noting charges are borne by ______________

(a) Notary Public

(b) Drawee

(c) Drawer

(d) Endorsee

Answer:

(b) Drawee

Question 6.

There are ______________ parties to bill of exchange.

(a) five

(b) four

(c) three

(d) two

Answer:

(c) three

![]()

Question 7.

When a bill is drawn for 2 months after date on 3rd Jan. 2020, its due date will be ______________

(a) 3rd Jan. 2020

(b) 3rd Mar. 2020

(c) 5th Mar. 2020

(d) 6th Mar. 2020

Answer:

(d) 6th Mar. 2020

Question 8.

Notary Public is ______________

(a) Govt. Officer

(b) Drawer

(c) Payee

(d) Endorsee

Answer:

(a) Govt. Officer

Question 9.

When Acceptor or Drawee does not pay the amount of bill to the holder on the due date it is known as ______________ the bill.

(a) returning

(b) discounting

(c) honouring

(d) dishonouring

Answer:

(d) dishonouring

Question 10.

The person who accepts the bill treats the bill as ______________

(a) Bills Payable

(b) Promissory Note

(c) Draft

(d) Bills Receivable

Answer:

(a) Bills Payable

B. Write the word/phrase/term, which can substitute each of the following statements:

Question 1.

Three extra days are allowed over and above the term of the bill.

Answer:

Grace days

Question 2.

Fees charged by Notary Public for getting the fact of dishonour noted.

Answer:

Noting Charges

Question 3.

A person who is entitled to receive the amount of bill of exchange.

Answer:

Payee

![]()

Question 4.

A person in whose favour a bill endorsed.

Answer:

Endorsee

Question 5.

Officer appointed by the government for noting of dishonour of bill.

Answer:

Notary Public

Question 6.

Cancellation of the bill on maturity in return for a new bill for an extended period of credit.

Answer:

Renewal of Bill

Question 7.

Bill of exchange drawn and accepted without any valuable consideration.

Answer:

Accommodation bill

Question 8.

A person who is in possession of the Bill of Exchange.

Answer:

Holder

Question 9.

Conversion of Bill of Exchange into its present value.

Answer:

Discounting of the bill

![]()

Question 10.

The amount is not recoverable from Drawee on account of insolvency.

Answer:

Bad debts

C. State whether the following statements are True or False with reasons:

Question 1.

An Inland bill is one that is drawn in one country and payable in another country.

Answer:

This statement is False.

Inland bill means, a bill drawn, accepted, and made payable within the territory of one and same, country. So, a bill is drawn in one country and payable in another country can’t be an inland bill.

Question 2.

Retirement of the bill means payment of the bill before the due date.

Answer:

This statement is True.

Payment of the bill, by the acceptor of the bill to the holder of the bill before the due date, is known as Retirement of the bill. So retirement of the bill means payment of the bill before the due date.

Question 3.

Drawee can transfer the ownership of the bill.

Answer:

This statement is False.

Drawee is a debtor. He has to pay the amount of the bill to its holder on the due date. Hence he cannot transfer its ownership to other people. The drawer can transfer the ownership of the bill as he is the owner of the bill.

Question 4.

Acceptance of the bill without making any changes in the terms of the bill is called qualified acceptance.

Answer:

This statement is False.

Acceptance of the bill with some changes as regards the terms, amount, place, etc. of a bill is known as qualified acceptance. Acceptance of the bill without making changes as regards the term is called general acceptance.

![]()

Question 5.

Discounting is a device to convert the bill into its present value.

Answer:

This statement is True.

When the drawer or holder of the bill approaches the bank to discount the bill, the bank pays the bill amount after deducting a certain amount (which is known as discounting charges). It means conversion of the bill into its present value in cash. So, we can say that discounting is a device to convert the bill into its present value.

Question 6.

A bill of exchange must be presented to the acceptor on the due date.

Answer:

This statement is True.

To get the payment of the bill from the acceptor, the holder of the bill is required to present it to the acceptor on its due date. Acceptor either honours the bill or dishonours the bill.

Question 7.

If a bill is discounted by the holder, no entry is passed in his book when the bill is honoured on the due date.

Answer:

This statement is True.

On discounting the bill the holder gives the possession of the bill to the bank. On the maturity date, the bank has to present the bill to the drawee to collect the payment. When the discounted bill is honoured, the transaction takes place between drawee and bank.

Question 8.

Noting charges are to be borne by the drawer.

Answer:

This statement is False.

Noting charges are to be borne by the drawee only as due to his act of non-payment, the bill is dishonoured and the drawer is not able to get money on its due date.

Question 9.

If a bill is drawn payable ‘on demand’ no grace days are allowed.

Answer:

This statement is True.

‘On demand’ means the amount of the bill is to be paid by drawee immediately on presentation of the bill as no time period is mentioned on it. In demand bill, 3 days grace is not allowed by law.

![]()

Question 10.

There are three parties to a promissory note.

Answer:

This statement is False.

There are only two parties to a promissory note, i.e. Drawer or maker of the note and drawee or payee of the note.

D. Find the odd one:

Question 1.

(a) Retaining

(b) Noting

(c) Discounting

(d) Endorsing

Answer:

(b) Noting

Question 2.

(a) Trade bill

(b) Accommodation bill

(c) After date bill

(d) Demand bill

Answer:

(d) Demand bill

Question 3.

(a) Notary public

(b) Drawer

(c) Drawee

(d) Payee

Answer:

(a) Notary public

![]()

Question 4.

(a) Discounting charges

(b) Rebate

(c) Bank charges

(d) Noting charges

Answer:

(d) Noting charges

Question 5.

(a) Stamp

(b) Acceptance

(c) Draft

(d) Amount

Answer:

(c) Draft

E. Complete the sentences:

Question 1.

Making payment of bill before the due date of maturity is known as ______________

Answer:

Retirement of Bill

Question 2.

A person whose liabilities are more than his assets and is not in a position to pay off his liabilities is ______________

Answer:

Insolvent person

Question 3.

Amount that cannot be paid by acceptor on account of insolvency is known as ______________

Answer:

Deficiency

Question 4.

A bill of exchange payable after certain period is known as ______________

Answer:

After date bill

![]()

Question 5.

A bill which is drawn and accepted with valuable consideration is known as ______________

Answer:

Trade Bill

Question 6.

A person who draws the bill of exchange is known as ______________

Answer:

Drawer

Question 7.

A bill whose due date is calculated from the date of acceptance is known as ______________

Answer:

After sight bill

Question 8.

Recording the fact of dishonour of bill is known as ______________

Answer:

Noting

Question 9.

When drawee accepts the bill payable at a particular place only, it is known as ______________

Answer:

qualified acceptance as to place

![]()

Question 10.

Fees charged by the bank for collection of bill on behalf of holder is ______________

Answer:

bank charges

F. Answer in a sentence:

Question 1.

What do you mean by Bill of Exchange?

Answer:

A Bill of Exchange is a written order signed by the drawer, directing a certain person to pay a certain sum of money on-demand or on a certain future date to a certain person or as per his order.

Question 2.

What are Days of Grace?

Answer:

The three extra days allowed to the drawee or the acceptor of a bill for making payment on it are called Days of Grace.

Question 3.

What do you mean by Discounting a Bill of Exchange?

Answer:

Encashment of a bill of exchange with the bank for certain cash which is less than the face value of the bill, before its due date by its drawer or holder is called Discounting of a Bill of Exchange.

Question 4.

What is Noting of the Bill?

Answer:

Noting of a Bill of Exchange is the recording of the facts of its dishonour by a Notary public.

![]()

Question 5.

What are Noting Charges?

Answer:

Noting Charges are the fees charged by the Notary public for noting the facts of dishonour on the face of the bill and in his official register.

Question 6.

What is the relationship between drawer and drawee?

Answer:

The relationship between the drawer and the drawee is that of the creditor and debtor.

Question 7.

Who is the Payee of the Bill?

Answer:

The Payee of a Bill is the person to whom the bill is made payable or in whose favour the bill is drawn.

Question 8.

What do you mean by Rebate?

Answer:

Any concession or discount in monetary terms given by the holder of the bill of exchange to the drawee or acceptor, when a bill is retired is called a Rebate.

Question 9.

What is the Legal Due Date?

Answer:

The date which is arrived at after adding three days of grace to the nominal due date is known as Legal Due Date.

![]()

Question 10.

What are Bills Payable on Demand?

Answer:

When the amount of bill is payable by a drawee on the presentation of a bill, in which time period is not mentioned and grace days are not allowed is known as Bills Payable on Demand.

G. Do you agree or disagree with the following statements:

Question 1.

A bill of exchange is a conditional order.

Answer:

Disagree

Question 2.

The party which is ordered to pay the amount is known as the payee.

Answer:

Disagree

Question 3.

The person in whose favour the bill is endorsed is known as the endorsee.

Answer:

Agree

Question 4.

Rebate or discount given on retiring a bill is an income to the Drawee.

Answer:

Agree

![]()

Question 5.

A bill from the point of view of the debtor is called Bills payable.

Answer:

Agree

Question 6.

In case of bill drawn payable ‘on demand,’ no grace days are allowed.

Answer:

Agree

Question 7.

A bill is required to be accepted by Drawer.

Answer:

Disagree

Question 8.

A bill of exchange need not be dated.

Answer:

Disagree

Question 9.

A bill before acceptance is called Promissory Note.

Answer:

Disagree

![]()

Question 10.

Renewal is requested by the drawee to extend the credit period of the bill.

Answer:

Agree

H. Calculations:

Question 1.

Ganesh draws a bill for ₹ 40,260 on 15th Jan. 2020 for 50 days. He discounted the bill with the Bank of India @ 15 % p.a. on the same day. Calculate the amount of discount.

Solution:

Discount = Amount of Bill × \(\frac{\text { Rate }}{100} \times \frac{\text { Unexpired days }}{366}\)

= 40,260 × \(\frac{15}{100} \times \frac{50}{366}\)

= ₹ 825

(Note: 2020 is a Leap year, so the total number of days = 366)

Question 2.

Shefali Traders drew a bill on Maya for ₹ 30,000 on 1st Oct. 2019 payable after 3 months.

Calculate the amount of discount in the following cases:

(i) Shefali Traders discounted the bill on the same day @ 12 % p.a.

(ii) Shefali Traders discounted the bill on 1st Nov. 2019 @ 12 % p.a.

(iii) Shefali Traders discounted the bill on 1st Dec. 2019 @ 12 % p.a.

Solution:

Discount = Amount of Bill × \(\frac{\text { Rate }}{100} \times \frac{\text { Unexpired days }}{365}\)

(i) Discount = 30,000 × \(\frac{12}{100} \times \frac{3}{12}\) = ₹ 900

(ii) Discount = 30,000 × \(\frac{12}{100} \times \frac{2}{12}\) = ₹ 600

(iii) Discount = 30,000 × \(\frac{12}{100} \times \frac{1}{12}\) = ₹ 300

Question 3.

Veena who had accepted Sudha’s bill for ₹ 28,000 was declared bankrupt and only 35 paise in a rupee could be recovered from her estate. Calculate the amount of bad debts.

Solution:

From Veena, only 35 paise in a rupee could be recovered i.e. 65 paise in a rupee is bad debt for Sudha. So 65% of ₹ 28,000 = ₹ 18,200 is the amount of bad debts.

![]()

Question 4.

Nitin renewed his acceptance for ₹ 72,000 by paying ₹ 22,000 in cash and accepting a new bill for the balance plus interest @ 18%. p.a. for 4 months. Calculate the amount of the new bill.

Selution:

For Nitin,

Total outstanding = ₹ 72,000

Nitin paid in cash= ₹ 22,000

Remaining dues = ₹ 50,000

Now, on this ₹ 50,000 we have to calculate interest @ 18% for 4 months

I = \(\frac{\mathrm{PRN}}{100}\)

= 50,000 × \(\frac{18}{100} \times \frac{4}{12}\)

= ₹ 3,000

So, amount of new bill = Remaining dues + Interest

= 50,000 + 3,000

= ₹ 53,000

Question 5.

Nisha’s acceptance for ₹ 16,850 sent to the bank for the collection was honoured and bank charges debited were ₹ 125. Find out the amount actually received by Drawer.

Solution:

Bill of ₹ 16,850 sent to the bank for collection and it is honoured and bank charges = ₹ 125

So, actual amount received by drawer = 16,850 – 125 = ₹ 16,725.

Question 6.

A bill of ₹ 16,000 was drawn by Keshav on Gopal on 12th June 2019 for 2 months, what will be the due date, if all of sudden, the legal due date is declared as an emergency holiday?

Solution:

Consider immediate or next working day as the due date in case the legal due date is declared as an emergency holiday.

∴ The legal due date is 16th August 2019 (The next day).

![]()

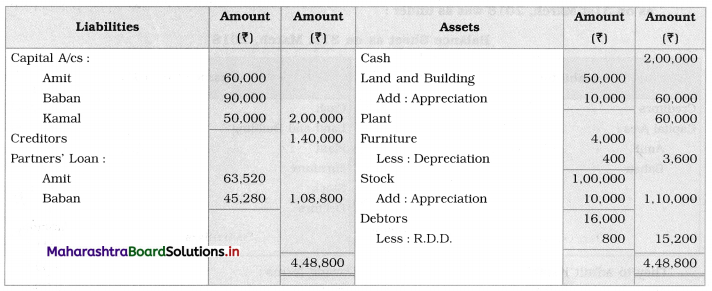

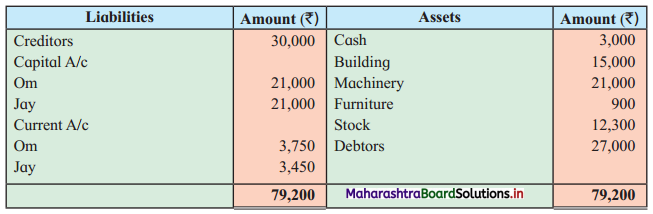

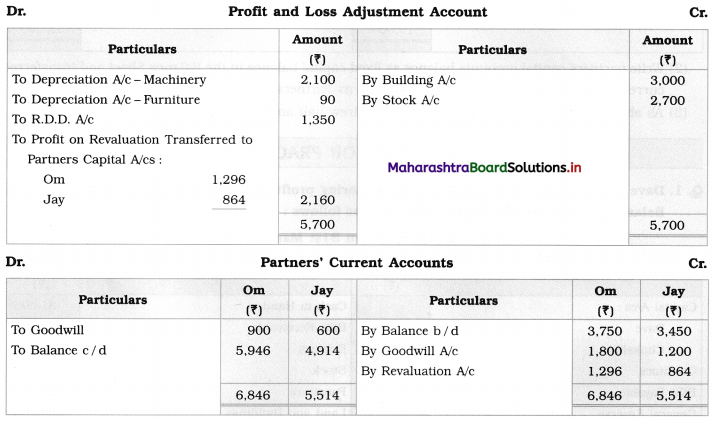

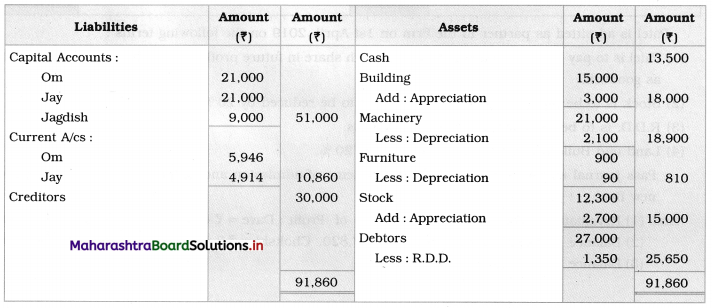

I. Prepare the following specimens:

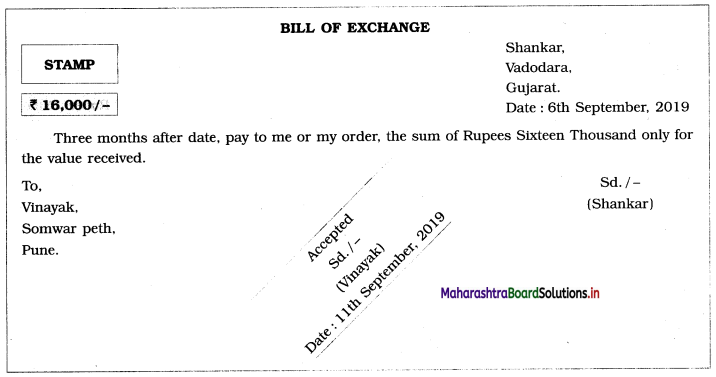

Question 1.

Prepare a bill of exchange from the following information:

Drawer: Shankar, Vadodara, Gujarat

Drawee: Vinayak, Somwar Peth, Pune

Amount: ₹ 16,000

Period: 3 months

Date of Bill: 6th Sept. 2019

Date of acceptance: 11th Sept. 2019

Solution:

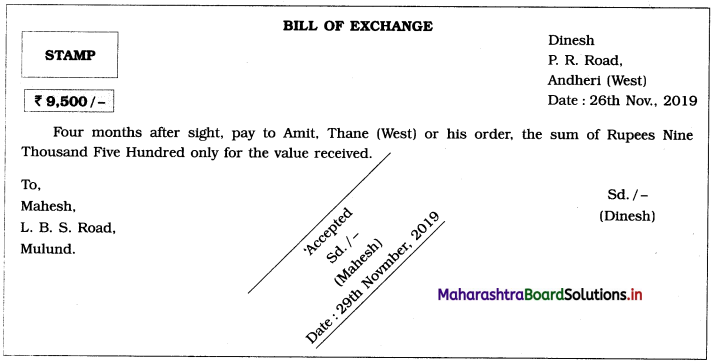

Question 2.

Prepare a bill of exchange from the following information:

Drawer: Dinesh, P. R. Road, Andheri (West)

Drawee: Mahesh, L. B. S. Road, Mulund

Payee: Amit, Thane (West)

Amount: ₹ 9,500

Period of Bill: 4 months after sight

Date of Bill: 26th Nov. 2019

Date of acceptance: 29th Nov. 2019

Solution:

![]()

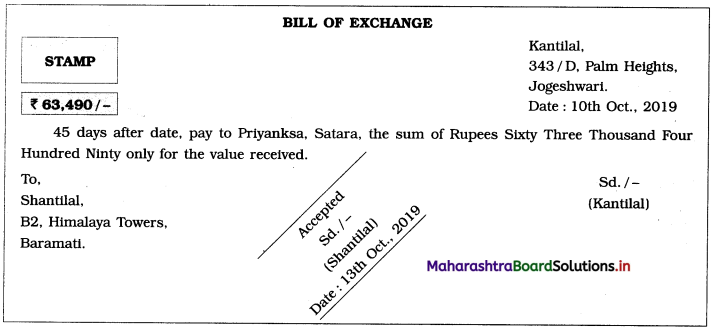

Question 3.

Kantilal, 343/D, Palm Heights, Jogeshwari, drew a bill on 10th Oct. 2019 for ₹ 63,490 for 45 days after the date on Shantilal, B2, Himalaya Towers, Baramati, payable to Priyanka, Satara. The bill was accepted on 13th Oct. 2019 for 60 days.

Prepare a format of bill of exchange from the above details.

Solution:

Question 4.

Prepare a format of bill exchange from the following:

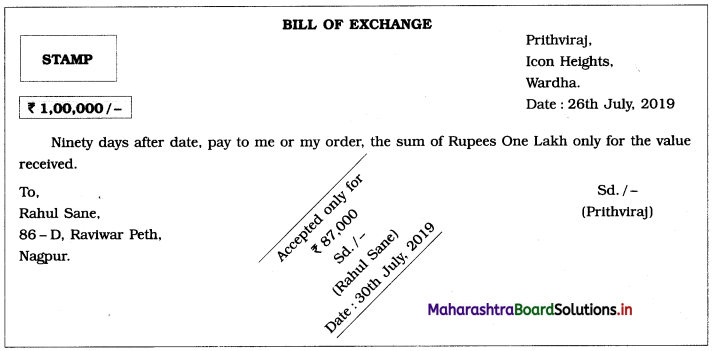

Rahul Sane, 86-D, Raviwar Peth, Nagpur accepted the bill drawn on him by Prithviraj, Icon Heights, Wardha for ₹ 87,000 on 30th July 2019.

The bill was drawn on 26th July 2019 for ₹ 1,00,000 for 90 days after the date.

Solution:

Question 5.

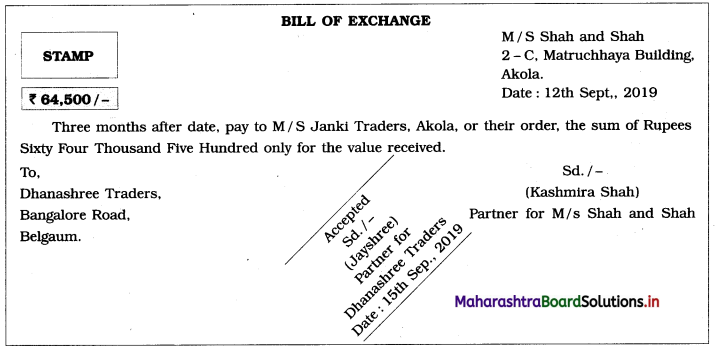

Prepare a format of bill of exchange from the following.

Drawer: Kashmira Shah, Partner M/S Shah, and Shah, 2 – C, Matruchhaya Building, Akola

Drawee: Dhanashree Traders, Bangalore Road, Belgaum (Signed by Jayshree, Partner)

Payee: M/S Janki Traders, Akola

Amount: ₹ 64,500

Period of Bill: 3 months

Date of drawing: 12th Sept. 2019

Date of acceptance: 15th Sept. 2019

Solution:

![]()

Question 6.

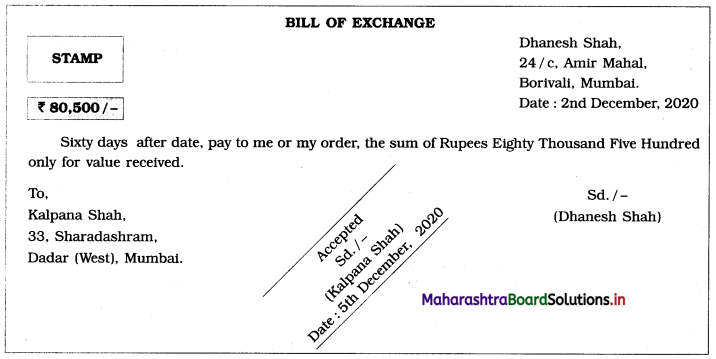

Prepare a format Bill of Exchange with imaginary Drawer, Drawee, Address, Amount, Dates.

Drawer: Dhanesh Shah, 24/c, Amir Mahal, Borivali, Mumbai

Drawee: Kalpana Shah, 33, Sharadashram, Dadar (West), Mumbai

Amount: ₹ 80,500

Period: 60 days

Date of the bill: 2nd December 2020

Accepted on: 5th December 2020

Solution:

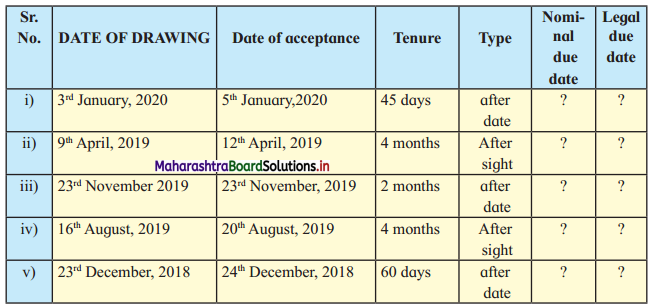

J. Complete the following Table.

Question 1.

Answer:

Question 2.

Answer:

| S.No. | Date of Drawing | Date of Acceptance | Tenure | Type | Nominal due Date | Legal due Date |

| (i) | 3rd January, 2020 | 5th January, 2020 | 45 days | after date | 17th Feb. 2020 | 20th Feb. 2020 |

| (ii) | 9th April, 2019 | 12th April, 2019 | 4 months | after sight | 12th Aug. 2019 | 14th Aug. 2019 |

| (iii) | 23rd November, 2019 | 23rd November, 2019 | 2 months | after date | 23rd Jan. 2020 | 25th Jan. 2020 |

| (iv) | 16th August, 2019 | 20th August, 2019 | 4 months | after sight | 20th Dec. 2019 | 23rd Dec. 2019 |

| (v) | 23rd December, 2018 | 24th December, 2018 | 60 days | after date | 21st Feb. 2019 | 24th Feb. 2019 |

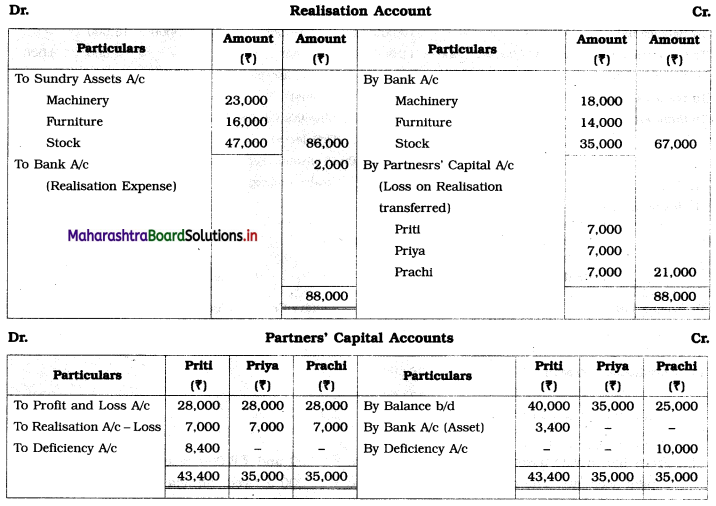

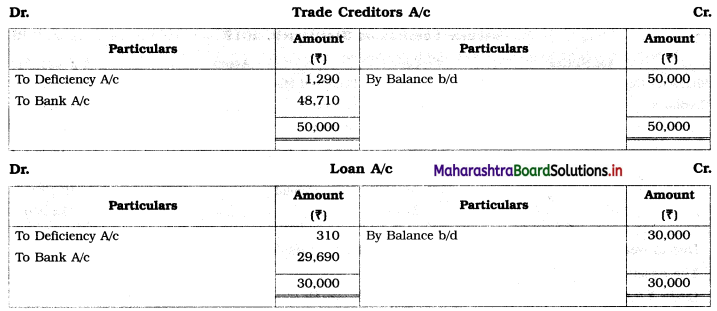

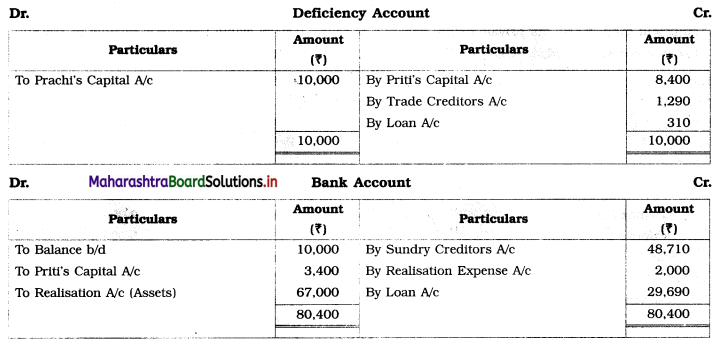

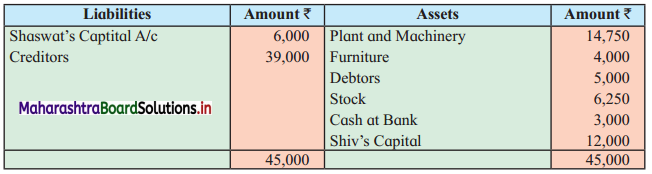

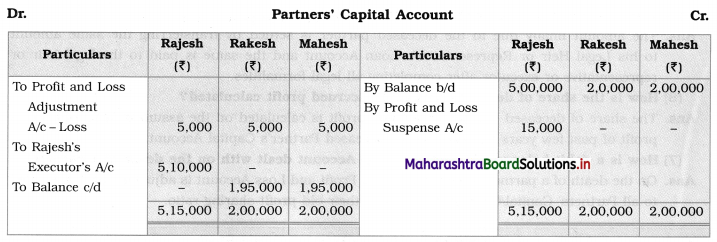

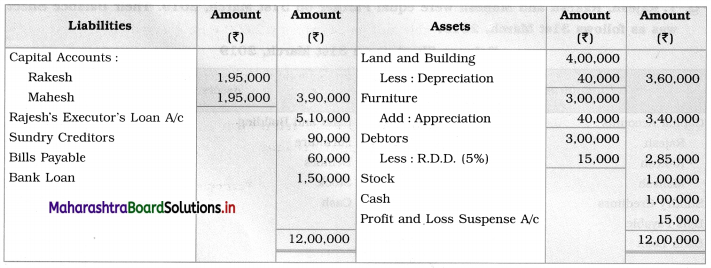

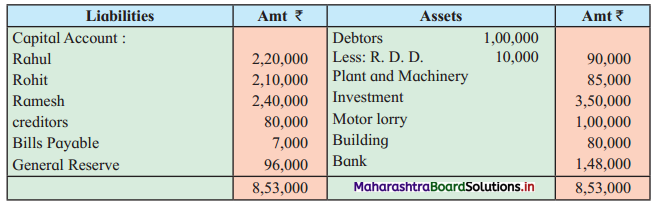

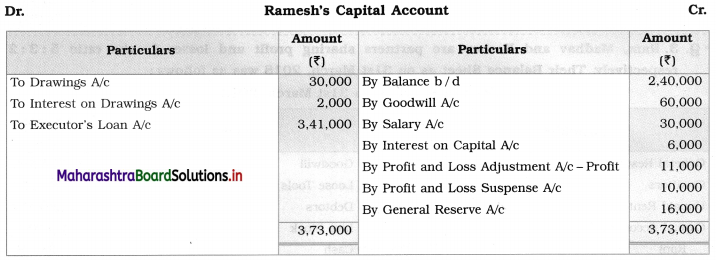

Practical Problems

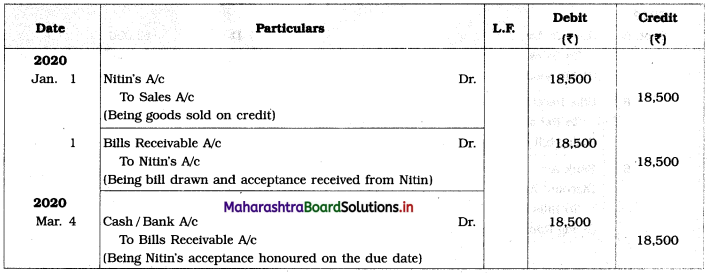

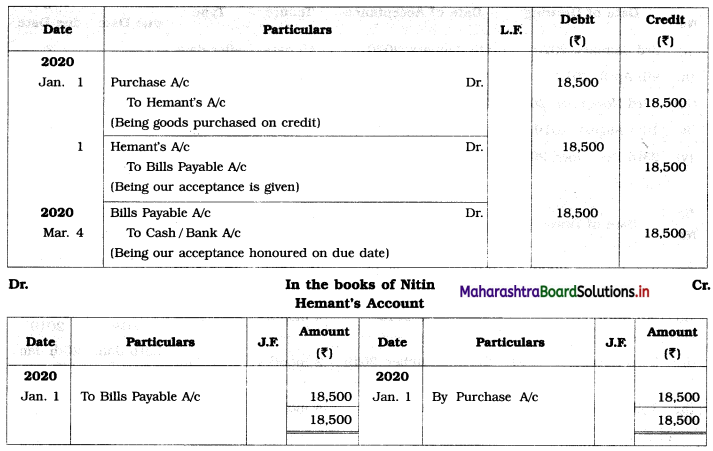

Question 1.

On 1st Jan., 2020 Hemant sold goods of ₹ 18,500 to Nitin. On the same date Hemant drew a bill of exchange for ₹ 18,500 at 2 months. On the due date the bill was duly honoured.

Give Journal Entries in the books of Hemant and Nitin. Prepare Hamant’s Account in the books of Nitin.

Solution:

In the books of Hemant

Journal Entries

In the books of Nitin

Journal Entries

![]()

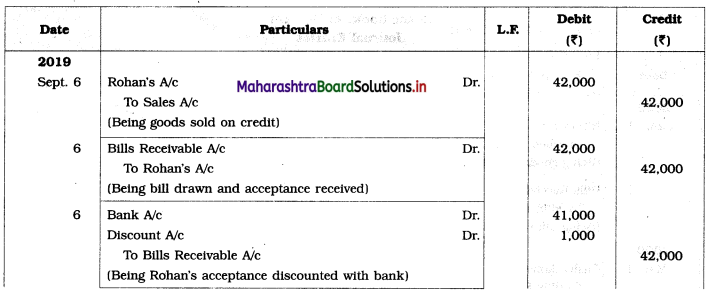

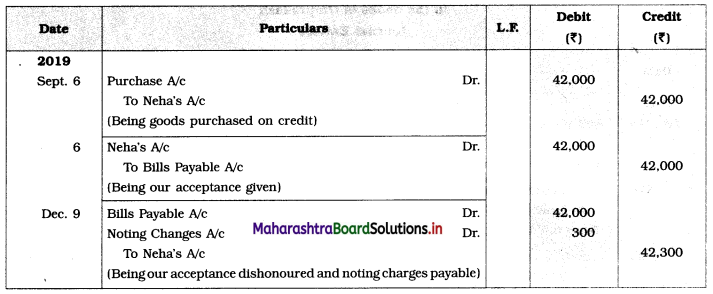

Question 2.

Neha sold goods to Rohan ₹ 42,000 on 6th Sept. 2019. Neha drew a bill of exchange at 3 months for the amount which was accepted by Rohan. Neha discounted the bill with her bankers at ₹ 41,000. On the due date of the bill Rohan dishonoured the bill and bank paid ₹ 300 as Noting Charges.

Show Journal Entries in the books of Neha and Rohan.

Solution:

In the books of Neha

Journal Entries

In the books of Rohan

Journal Entries

Question 3.

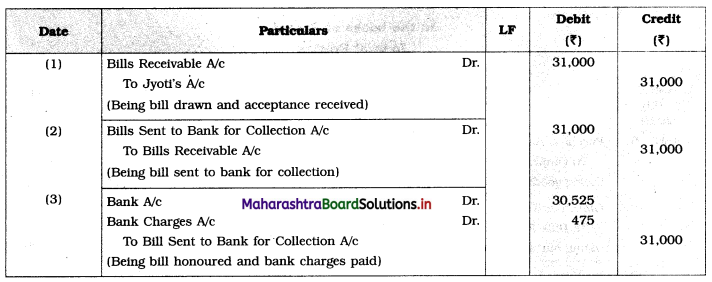

Jyoti owes ₹ 31,000 to Swati for which she draws a bill on Jyoti for 2 months. The bill was duly accepted by Jyoti. Swati sends the bill to bank for collection. Jyoti honoured the bill on the due date and bank charges ₹ 475 as bank charges.

Give Journal Entries in the books of Swati.

Solution:

In the books of Swati

Journal Entries

![]()

Question 4.

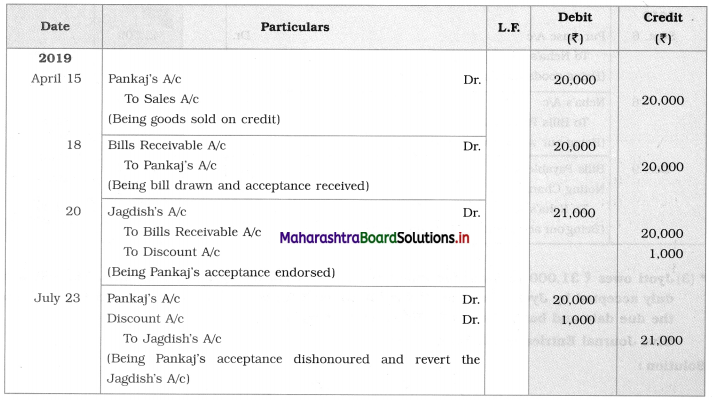

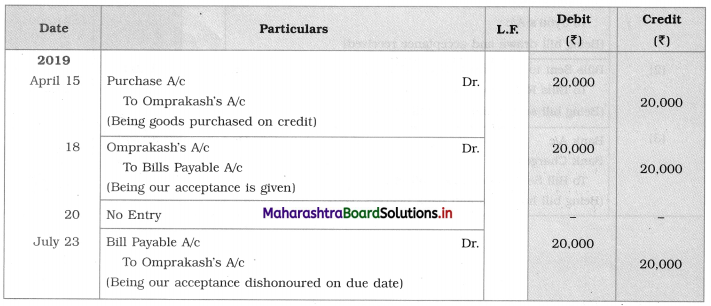

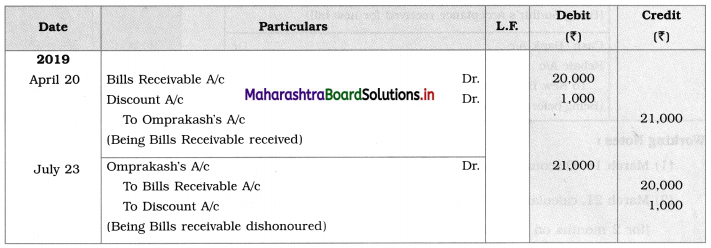

Pankaj purchased goods of ₹ 20,000 from Omprakash on credit on 15th April, 2019. Omprakash draws After Sight bill for the amount due on Pankaj for 3 months which was accepted by Pankaj on 18th April, 2019. On 20th April, 2019 Omprakash endorsed the bill to his creditor Jagdish in full settlement of his amount ₹ 21,000. On the due date the bill was dishonoured by Pankaj.

Give Journal Entries in the books of Omprakash, Pankaj and Jagdish.

Solution:

In the books of Omprakash

Journal Entries

In the books of Pankaj

Journal Entries

In the books of Jagdish

Journal Entries

Question 5.

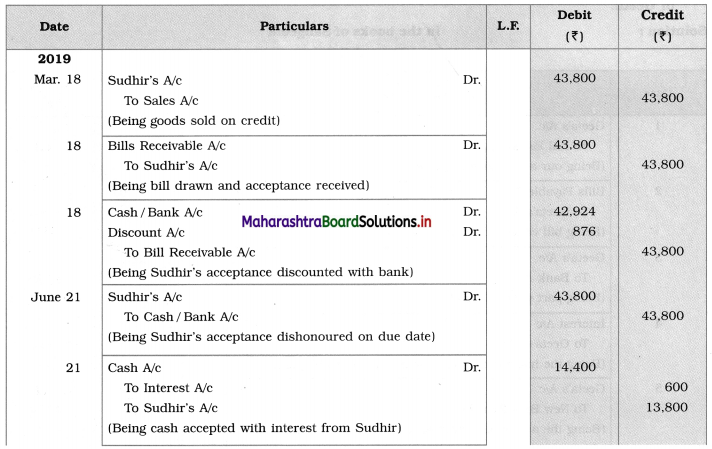

Siddhant sold goods to Sudhir of ₹ 43,800 on 18th March, 2019. Siddhant draws a bill on Sudhir on the same day for ₹ 43,800 for 3 months which was duly accepted by Sudhir. Siddhant discounted the bill on the same day at 8% p.a. The bill was dishonoured on the due date and Sudhir requested Siddhant to accept ₹ 13,800 and interest in cash on remaining amount at 12% p. a. Siddhant agreed and for the balance amount accepted a new bill at 2 months. Before the due date of new bill Sudhir retired the bill by paying ₹ 29,700.

Pass necessary Journal Entries in the books of Siddhant.

Solution:

In the books of Siddhant

Journal Entries

Working Notes:

1. March 18, Discount = 43,800 × \(\frac{3}{12} \times \frac{8}{100}\) = ₹ 876

2. March 21, calculation of interest balance amount:

I = \(\frac{\mathrm{PRN}}{100}\)

= 30,000 × \(\frac{12}{100} \times \frac{2}{12}\) (for 2 months on remaining amount ₹ 30,000)

= ₹ 600

3. Before due date bill was retired by Sudhir by paying ₹ 300 less which is considered as discount and as date is not given, here it is not recorded.

![]()

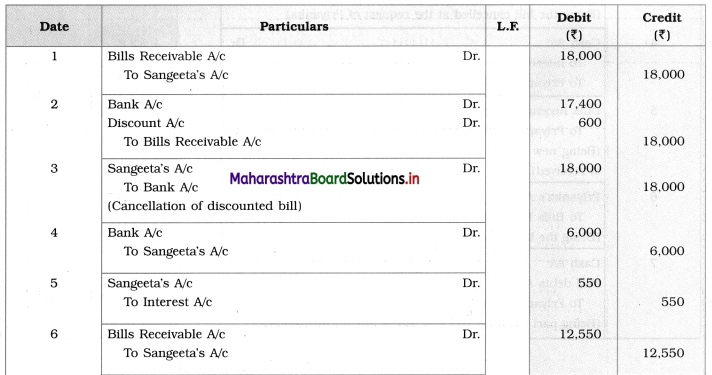

Question 6.

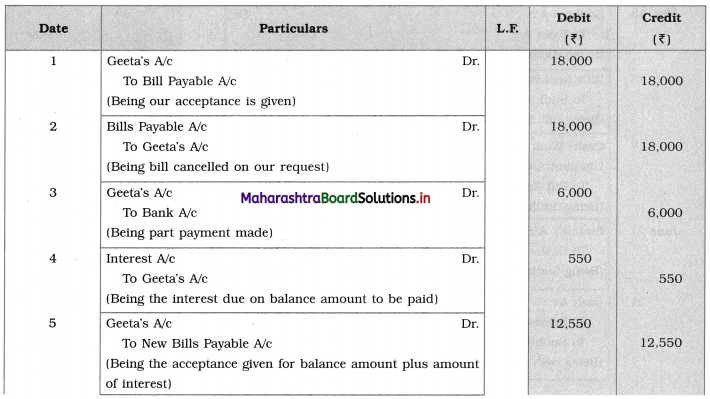

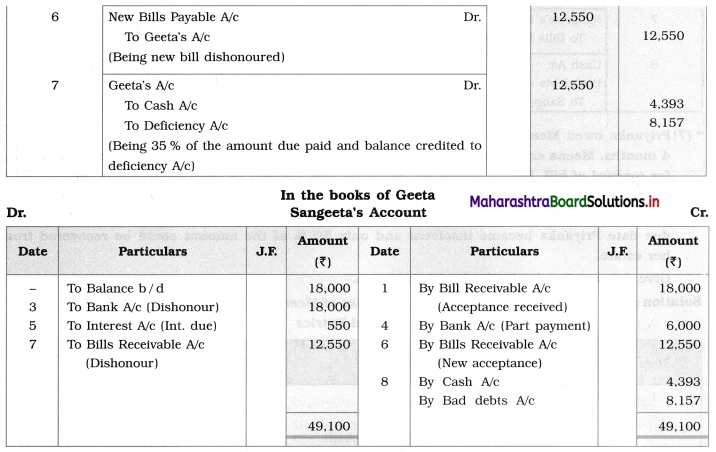

Sangeeta accepted a bill for ₹ 18,000 drawn by Geeta at 3 months. Geeta discounted the bill for ₹ 17,400. Before the due date Sangeeta approached Geeta for renewal of the bill. Geeta agreed on the condition that Sangeeta should pay ₹ 6,000 immediately and for the balance she should accept a new bill for 4 months along with interest ₹ 550. The arrangements were carried through. But on the due date of new bill Sangeeta became insolvent and 35 paise in a rupee could be recovered from her estate.

Give Journal Entries in the books of Sangeeta and prepare Sangeeta’s Account in the books of Geeta.

Solution:

In the books of Sangeeta

Journal Entries

Working Notes:

1. It is advisable to write journal entries in the books of Geeta also to get entries in ‘Sangeeta’s Account’ property.

In the books of Geeta

Journal Entries

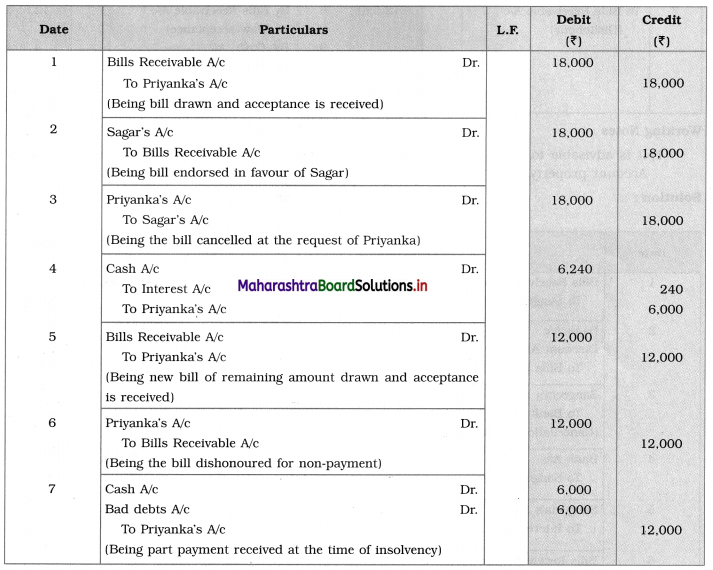

Question 7.

Priyanka owed Meena ₹ 18,000, Priyanka accepted a bill drawn by Meena for the amount at 4 months. Meena endorsed the same bill to Sagar. Before due date Priyanka approached Meena for renewal of bill. Meena agreed on condition that ₹ 6,000 be paid immediately together with interest on the remaining amount of 8% p.a. for 3 months and Priyanka should accept a new bill for the balance amount. These arrangements were carried through. However, before the due date Priyanka became insolvent and only 50% of the amount could be recovered from her estate.

Give Journal Entries in the books of Meena.

Solution:

In the books of Meena

Journal Entries

Working Note:

Calculation of interest on remaining amount ₹ 12,000 @ 8 % p.a. and for 3 months

I = \(\frac{\mathrm{PRN}}{100}\)

= 12,000 × \(\frac{8}{100} \times \frac{3}{12}\)

= ₹ 240

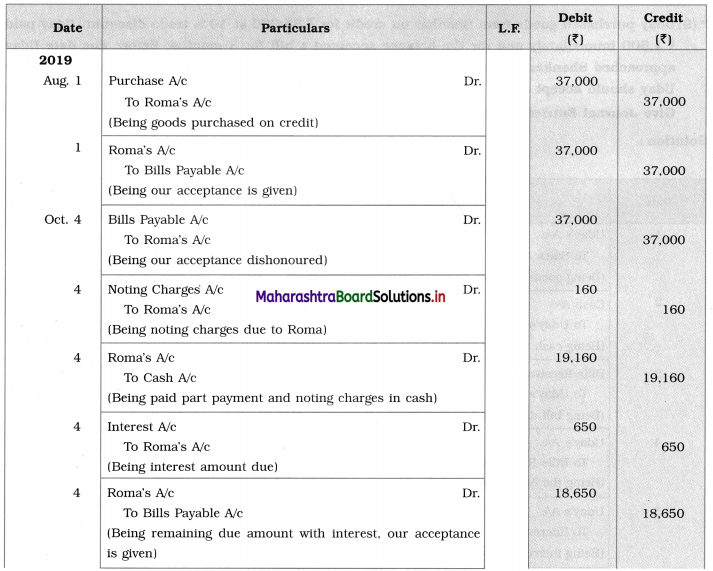

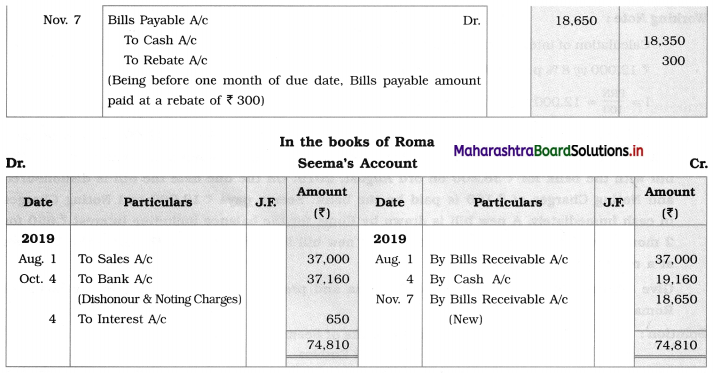

Question 8.

Seema purchased goods from Roma on credit on 1st August, 2019 for ₹ 37,000. Seema accepts bill for 2 months drawn by Roma for the same amount. On the same day, Roma discounts the bill with the bank for ₹ 36,200 on 3rd August, 2019. On the due date the bill is dishonoured and Noting Charges of ₹ 160 is paid by the bank. Seema pays ₹ 19,000 and Noting Charges in cash immediately. A new bill is drawn by Roma for the balance including interest ₹ 650 for 2 months, which is accepted by Seema. The new bill is retired one month before the due date at a rebate of ₹ 300.

Give Journal Entries in the books of Seema and prepare Seema’s Account in the books of Roma.

Solution:

In the books of Seema

Journal Entries

![]()

Question 9.

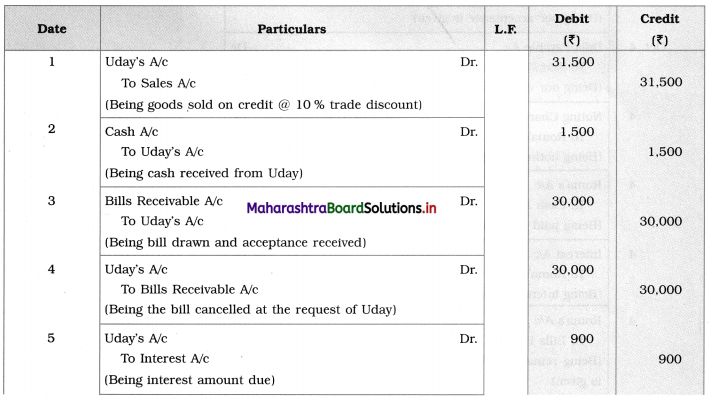

Uday purchased goods from Shankar on credit for ₹ 35,000 at 10 % trade discount. Uday paid ₹ 1,500 immediately and for the balance accepted a bill for 3 months. Before due date Uday approached Shankar with a request to renew the bill. Shankar agreed but with condition that Uday should accept a new bill for 3 months including interest at 12% p.a.

Give Journal Entries in the books of Shankar.

Solution:

In the books of Shankar

Journal Entries

Working Note:

I = \(\frac{\text { PRN }}{100}\)

= 30,000 × \(\frac{3}{12} \times \frac{12}{100}\)

= ₹ 900

Question 10.

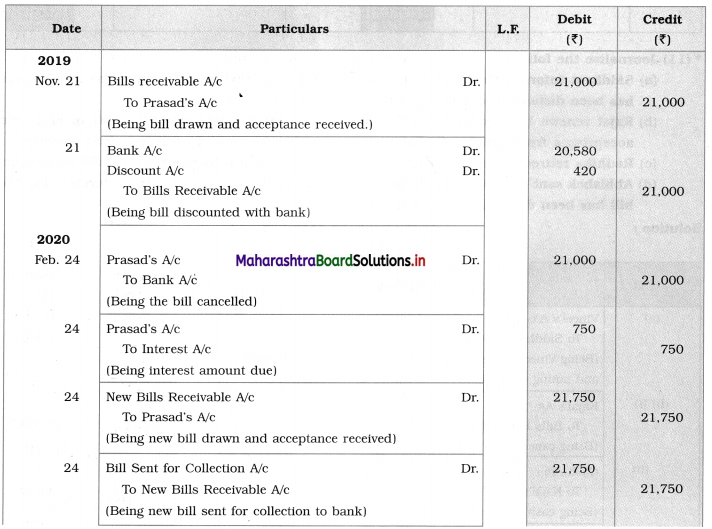

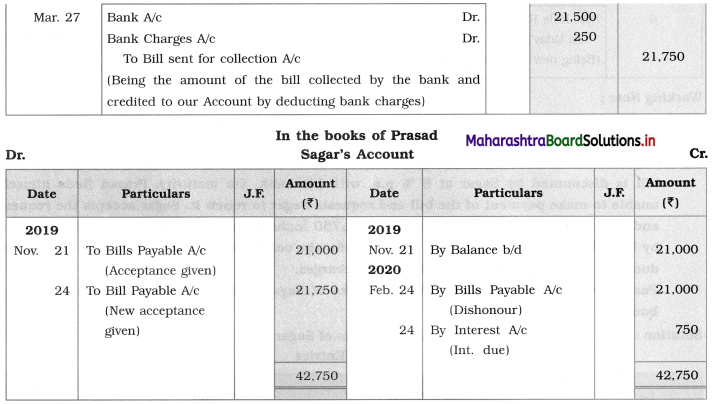

Sagar drawn an after sight bill on 21st Nov., 2019 for ₹ 21,000 at 3 months on Prasad. The bill is discounted by Sagar at 8% p.a. with his bank. On maturity. Prasad finds himself unable to make payment of the bill and requests Sagar to renew it. Sagar accepts the request and draws a new bill at one month for ₹ 21,750 including interest which was duly accepted by Prasad. Sagar deposits the bill into bank for the collection. Prasad honours the bill on the due date and bank charges ₹ 250 as bank charges.

Pass necessary Journal Entries in the books of Sagar and prepare Sagar’s Account in the books of Prasad.

Solution:

In the books of Sagar

Journal Entries

Question 11.

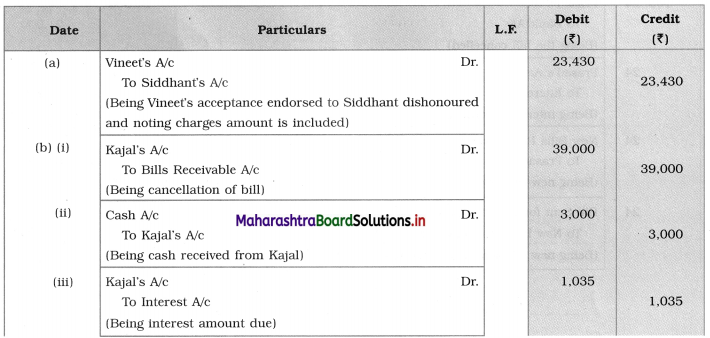

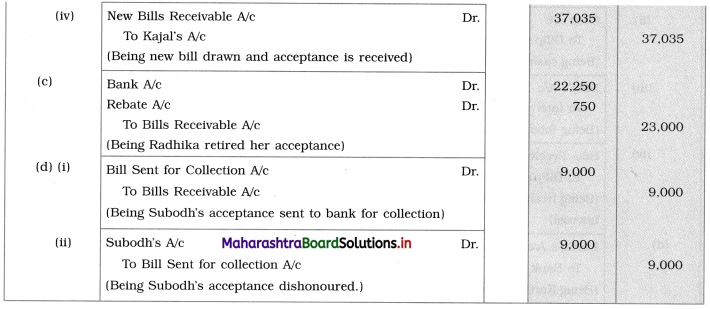

Journalise the following transaction in the books of Abhishek:

(a) Siddhant informs Abhishek that Vineet’s acceptance for ₹ 23,000 endorsed to Siddhant has been dishonoured. Noting Charges amounted to ₹ 430.

(b) Kajal renews her acceptance to Abhishek for ₹ 39,000 by paying ₹ 3,000 in cash and accepting a fresh bill for the balance along with interest at 11.5% p.a. for 3 months.

(c) Radhika retired her acceptance to Abhishek for ₹ 23,000 by paying ₹ 22,250 by cheque.

(d) Abhishek sent a bill of Subodh for ₹ 9,000 to bank for collection. Bank informed that the bill has been dishonoured by Subodh.

Solution:

In the books of Abhishek

Journal Entries

Working Note:

Amount of interest = 36,000 × \(\frac{3}{12} \times \frac{11.5}{100}\) = ₹ 1,035.

![]()

Question 12.

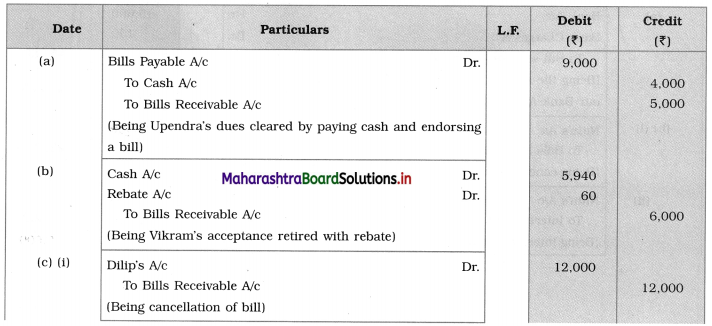

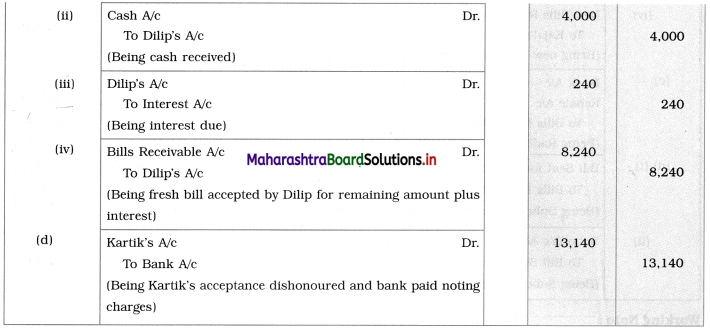

Journalise the following transaction in the books of Narendra:

(a) Narendra retires his acceptance to Upendra by paying ₹ 4,000 in cash and endorsing a bill accepted by Ramlal for ₹ 5,000.

(b) Vikram’s acceptance to Narendra ₹ 6,000 retired one month before the due date at rebate of 12% p.a.

(c) Dilip renews his acceptance to Narendra for ₹ 12,000 by paying ₹ 4,000 in cash and accepting a fresh bill for the balance plus interest at 12% p.a. for 3 months.

(d) Bank informed Narendra that, Kartik’s acceptance for ₹ 13,000 to Narendra, discounted with the bank was dishonoured and Noting Charges paid by bank ₹ 140.

Solution:

In the books of Narendra

Journal Entries

Question 13.

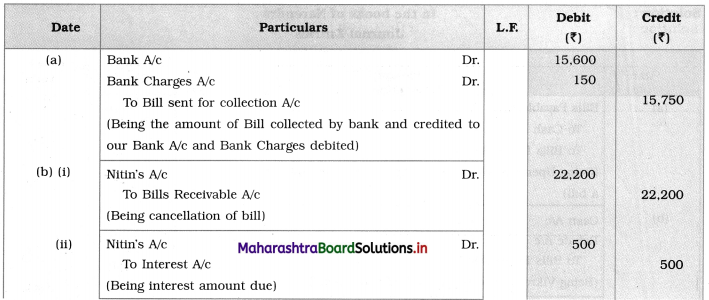

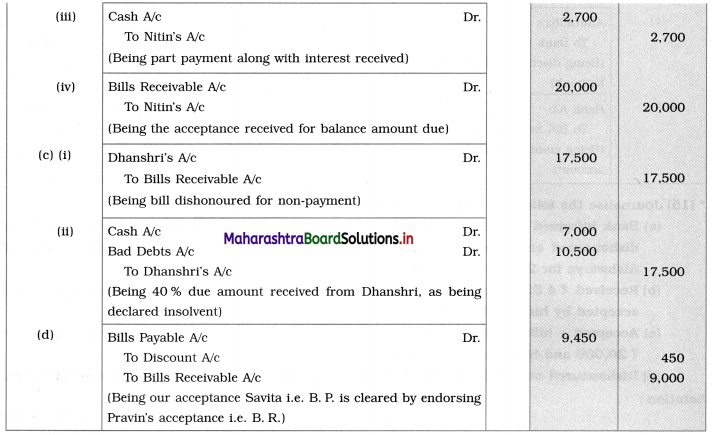

Journalise the following transaction in the books of Bharti:

(a) Bank informed that Amit’s acceptance for ₹ 15,750 sent to bank for collection was honoured and bank charges debited were ₹ 150.

(b) Nitin renewed his acceptance for ₹ 22,200 by paying ₹ 2,200 in cash along with interest on balance amount at 10% and accepted a fresh bill for the balance for 3 months.

(c) Dhanshri who had accepted Bharti’s bill for ₹ 17,500 was declared insolvent and only 40% of the amount due could be recovered from her estate.

(d) Discharged our acceptance to Savita for ₹ 9,450 by endorsing Pravin’s acceptance to us ₹ 9,000.

Solution:

In the books of Bharti

Journal Entries

Question 14.

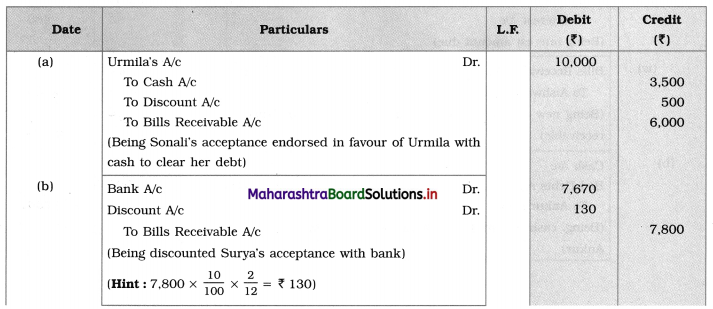

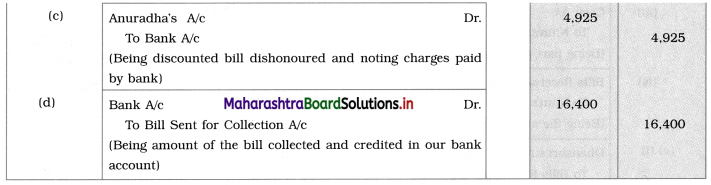

Journalise the following transaction in the books of Sudha:

(a) Endorsed Sonali’s acceptance at 2 months for ₹ 6,000 in favour of Urmila and paid cash ₹ 3,500 in full settlement of her account ₹ 10,000.

(b) Discounted 2 months acceptance of Surya for ₹ 7,800 with bank at 10% p.a.

(c) Bank informed that Anuradha’s acceptance of ₹ 4,800 which was discounted was dishonoured and bank paid Noting Charges ₹ 125.

(d) Pooja honoured her acceptance of ₹ 16,400 which was deposited into bank for collection.

Solution:

In the books of Sudha

Journal Entries

![]()

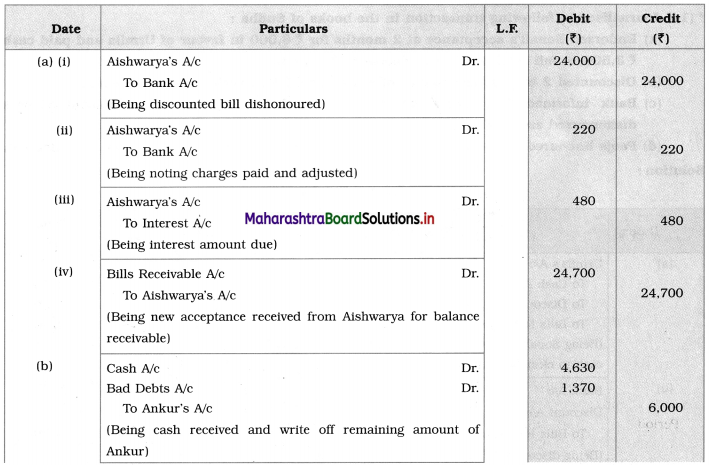

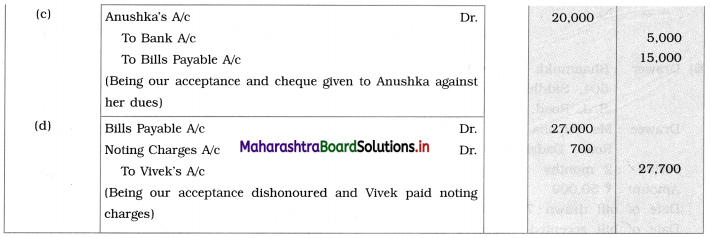

Question 15.

Journalise the following transaction in the books of Mrunal:

(a) Bank informed that Aishwarya’s acceptance of ₹ 24,000 which was discounted had been dishonoured and bank paid Noting Charges ₹ 220. Bill was renewed at the request of Aishwarya for 2 months with interest of ₹ 480.

(b) Received ₹ 4,630 from private estate of Ankur who was declared insolvent against bill accepted by him for ₹ 6,000.

(c) Accepted a bill of ₹ 15,000 at 3 months drawn by Anushka for the amount due to her ₹ 20,000 and balance paid by cheque.

(d) Dishonoured our acceptance to Vivek ₹ 27,000 and Noting Charges paid by Vivek ₹ 700.

Solution:

In the books of Mrunal

Journal Entries