Balbharti Maharashtra State Board Class 12 Economics Important Questions Chapter 5 Forms of Market Important Questions and Answers.

Maharashtra State Board 12th Economics Important Questions Chapter 5 Forms of Market

1. A. Choose the correct option:

Question 1.

Features of Perfect Competition are –

(a) Large number of buyers

(b) Large number of sellers

(c) Different prices

(d) Perfect mobility

Options :

(1) a, b and c

(2) a, b and d

(3) b, c and d

(4) c and d

Answer:

(2) a, b and d

Question 2.

Features of monopoly are –

(a) Single seller

(b) No close substitutes

(c) Control over supply

(d) Price taker

Options :

(1) a, b and d

(2) a, b, c and d

(3) c and d

(4) a, b and c

Answer:

(4) a, b and c

Question 3.

Features of Monopolistic Competition are –

(a) Homogeneous product

(b) Selling cost

(c) Downward sloping demand curve

(d) Few buyers

Options :

(1) b and c

(2) a, b and d

(3) c and d

(4) a, b and c

Answer:

(1) b and c

Question 4.

Legal monopoly is recognized by –

(a) Legal provision

(b) Trade Mark

(c) License

(d) Copyright

Options :

(1) a, b, c and d

(2) a, b and d

(3) a, b and c

(4) a and c

Answer:

(1) a, b, c and d

Question 5.

Examples of discriminating monopoly are –

(a) Doctors

(b) Lawyers

(c) Consultants

(d) All of the above

Options :

(1) a and d

(2) a, b and d

(3) a, b and c

(4) a, b, c and d

Answer:

(4) a, b, c and d

Question 6.

Types of imperfect market are –

(a) Monopoly

(b) Oligopoly

(c) Monopolistic Competition

(d) Perfect Competition

Options :

(1) b and c

(2) a, b and c

(3) only d

(4) all of these

Answer:

(2) a, b and c

(B) Complete the Correlation.

(1) Tata group : Private monopoly :: Indian Railways : ………………..

(2) Few sellers : Oligopoly :: Many sellers : ………………..

(3) Less than one year : Short period :: More than five years : ………………..

(4) Perfect competition : No selling cost :: Monopolistic competition : ………………..

(5) Natural monopoly : Wheat from Punjab :: ……………….. : Copy right

(6) Perfect competition : Homogeneous :: ……………….. : Differentiated products

(7). Theory of Monopolistic competition : Prof. Chamberlin :: Perfect competition : ………………..

(8) Perishable goods : Local market :: Non-perishable goods : ……………….

(9) OPEC : Group Monopoly :: RIL : ………………..

(10) Petroleum : ……………….. :: Scooter : National market.

Answers:

- Public monopoly

- Perfect competition

- Very long period

- Selling cost

- Legal monopoly

- Imperfect competition

- Mrs. Joan Robinson

- National Market

- Private monopoly

- International market

(C) Give economic terms.

- A monopoly recognised by law.

- The cost that can add to the price of the product in a distant market.

- A market in which laissez faire policy is adopted by the government.

- A network of dealings between buyers and sellers.

- A market in which a firm and industry are same.

- A monopoly that arises when a particular type of natural resources are located in a particular region.

- A price that is determined by intersection of demand and supply.

- Welfare oriented monopoly. Railways, Courier services, Water supply,

- A practice of charging different prices for the same product.

- A monopoly formed by an organisation of Petroleum Exporting countries.

- When there is no difference between the firm and industry.

Answer:

- Legal monopoly

- Transport cost

- Perfect competition

- Market

- Monopoly

- Natural monopoly

- Equilibrium price

- Public monopoly

- Price discrimination

- Voluntary monopoly

- Monopsony

(D) Find the odd word out

(1) Market structure on the basis of place :

Local, National, Oligopoly, International.

(2) Peculiarities of Perfect competition :

Many buyers, Few sellers, Price taker, No transport cost.

(3) Examples of Public Monopoly :

Railways, Courier services, Water supply, Electricity.

(4) Features of Monopoly :

Many sellers, Many buyers, Entry barriers to sellers, Firm coincides with industry.

(5) Natural Monopoly depends upon :

Climate, Rainfall, Specific location, Many sellers.

(6) Private monopoly :

Tata group, OPEC, Adani power, Post office.

(7) Imperfect competition :

Price discrimination, Uniform price, Barriers to entry, Price maker.

Answer:

- Oligopoly

- Few sellers

- Courier services

- Many sellers

- Many sellers

- Post office

- Uniform price

(E) Complete the following statements.

(1) Equilibrium price is that level of price where ………………

(2) A seller is price maker in ………………

(3) A welfare oriented monopoly is called ………………

(4) A Market in which sellers sell and buyers buy the product in the region in which it is produced is called ………………

(5) A market in which buyers and sellers trade in goods and services across the national borders is called ………………

(6) A classification of market on the basis of place are local, national and ………………

(7) A market on the basis of competition which is ideal and imaginary concept is called………………

(8) A market showing some but not all the features of a competitive market is called………………

(9) When a private body controls a monopoly firm, it is called ………………

(10) When the production is totally controlled and operated by the government it is known as………………

(11) Tea cultivation in Assam is an example of………………

(12) A firm which charges different prices to different buyers for the same product, it is called………………

(13) When some monopolists come together voluntarily to form a group of monopolists, it is called ………………

(14) Different brands of washing powders, liquid cleaners are examples of………………

(15) Selling cost is an important feature of………………

(16) Mobile service providers and cement companies are examples of ………………

(17) A period of production is so long that all inputs are variable is called ………………

(18) A market in which supply is fixed is called ………………

(19) A book “Theory of Monopolistic Competition is written by ………………

(20) The objective of the seller in monopoly market is ………………

(21) Under monopoly there is existence of ………………

Answer:

- market demand is equal to market supply

- monopoly .

- public monopoly

- local market

- international market

- international

- perfect competition

- imperfect market

- private monopoly

- public monopoly

- natural monopoly

- discriminating monopoly

- voluntary monopoly

- monopolistic competition

- monopolistic competition

- oligopoly market

- very long period market

- very short period market

- Prof. E. H. Chamberlin

- profit maximisation

- single seller

[F] Choose the wrong pair ;

I.

| Group ‘A’ | Group ‘B’ |

| 1. Perfect competition | Many buyers and sellers |

| 2. Oligopoly | Many buyers and few sellers |

| 3. Imperfect market | Monopoly, International market |

Answer:

3.

II.

| Group ‘A’ | Group ‘B’ |

| 1. Market on the basis of place | Local, National, International |

| 2. Market on the basis of competition | Perfect competition, International |

| 3. Market on the basis of time | Very short, short, long, Very long |

Answer:

2

III.

| Group ‘A’ | Group ‘B’ |

| 1. Public Monopoly | Wheat from Punjab |

| 2. Natural Monopoly | Tea from Assam |

| 3. Private Monopoly | Reliance Group |

Answer:

1

(G) Choose the correct pair

I.

| Group ‘A’ | Group ‘B’ |

| 1. Very short period | (a) More than 5 years |

| 2. Short period | (b) Less than 1 year |

| 3. Long period | (c)Few days or weeks |

| 4. Very long period | (d) Upto 5 years |

Answer:

(1)-(c), (2)-(b), (3)-(d), (4)-(a).

II.

| Group A | Group B |

| 1. Perfect Competition | (a) Product Differentiation |

| 2. Monopoly | (b) Uniform Price |

| 3. Monopolistic Competition | (c) Few Sellers |

| 4. Oligopoly | (d) Single Seller |

Answer:

(1)-(b), (2)-(d), (3)-(a), (4)-(c).

2.[A] Identify and explain the concept from given illustrations.

Question 1.

| Output sold in units | Price of ‘X’ in ₹ | Price of ‘Y‘ in ₹ |

| 100 | 50 | 50 |

| 200 | 50 | 40 |

| 300 | 50 | 30 |

Identify the type of market of two goods X’ and ‘Y’ Give reason for your answer.

Answer:

Concept : Market for good ‘X’ is perfect competition.

Explanation : At the same price ? 50 sellers are ready to sell more and more in the market.

Concept : Market for good ‘Y’ is

monopolistic competition.

Explanation : As price of ‘Y’ falls, more and more sellers enter the market to sell their product.

Question 2.

| Client | Elec, per unit by Government | Lawyer fee in ₹ |

| A | 10 | 1000 |

| B | 10 | 2000 |

| C | 10 | 3000 |

(1) Identify the type of monopoly by the government and Lawyer. Give reason for your answer.

Answer:

Concept: Electricity charges by government – Public Monopoly.

Explanation : Public monopoly is welfare oriented monopoly and is owned by the government. Therefore, their price per unit remains uniform.

Answer:

Concept : Lawyer fee – Discriminating Monopoly.

Explanation : In case of lawyer, being a private practitioner, he can charge different fee from different customers. Hence, it is called discriminating monopoly.

Question 3.

A washing powder seller incurs extra cost in order to give free samples to the customers as a sales strategy.

Answre:

Concept : Monopolistic Competition (Selling Cost).

Explanation : In this type of market, there are many sellers who sell the product which are close substitutes of each other.

As there are many variety of washing powders available in the market, he distributes free samples to attract the customers to buy his product.

Question 4.

“A monopoly firm can exercise considerable influence on the supply of his commodity and thereby its price.”

Answre:

Concept : Price Maker (Feature of Monopoly).

Explanation : A monopolist is a single seller in the market for his product and has control over the supply and can determine the price for his product.

There are no close substitutes available for his product in the market.

So, he is a price maker.

[B] Distinguish between :

(1) Perfect Competition and Monopoly.

Answer:

Perfect Competition:

- Perfect competition is a type of market where there are large number of firms producing homogeneous product.

- The product sold are homogeneous and so they are perfect substitutes.

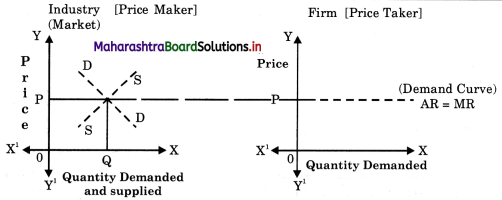

- The firm is a price taker so the demand curve is a horizontal demand curve.

- There is free entry and free exit.

- Single price prevails in the whole market.

Monopoly:

- Monopoly is a type of market where there is only one firm producing a product which has no substitute.

- The product has no substitute.

- The firm is a price maker. Thus firm has a downward sloping demand curve.

- There are strong entry barriers.

- Price discrimination is possible because seller has complete hold in the market.

Question 2.

Perfect Competition and Monopolistic Competition.

Answer:

Perfect Competition:

- It is a market situation in which there are large number of buyers and large number of sellers selling homogeneous product.

- Products are perfect substitute for another as they are identical.

- Uniform price prevails in the whole market. There is no selling cost.

- Firms are price takers. Thus the firm has a horizontal demand curve.

- It is an unrealistic market.

Monopolistic Competition:

- It is a market situation in which there are many buyers and many sellers selling differentiated products.

- Products are similar but not identical. They are close substitutes.

- Individual price policy is followed and huge selling cost is incurred on sales promotions.

- The firms are price makers. Thus the firms have a downward sloping demand curve.

- It is a realistic market.

Question 3.

Natural Monopoly and Social Monopoly.

Answer:

Natural Monopoly:

- The monopoly power is acquired by a firm due to natural advantages such as good location, control over scarce resources, natural skill, talent, etc.

- Natural monopoly is determined by the availability of natural resources or natural talents and skills.

- Normally the monopolist would charge higher prices for the goods.

- Main objective is to maximise profit.

- Gulf countries monopolies in production of oil. India’s monopoly in production of jute and cotton. Lata Mangeshkar monopolised as a professional singer once upon a time.

Social Monopoly / Public Monopoly:

- When government nationalises an industry and acquires complete control over its market that monopoly is called as social monopoly.

- Social monopoly is determined by economic aims and objectives of the government.

- Government may not charge higher prices keeping in mind the welfare aspect.

- The main objective is to provide social welfare.

- Public utility services like water supply, railway services etc., are examples of public monopoly.

Question 4.

Natural Monopoly and Legal Monopoly.

Answer:

Natural Monopoly:

- The monopoly power acquired by a firm due to natural advantages such as good location, control over scarce resources or natural skill, etc.

- The main objective of a natural monopolist is to maximise profits.

- Monopoly due to location or may be old establishment like the TATA products or Godrej Locks, Cupboards etc., or an actor like Amir Khan.

Legal Monopoly:

- It arises due to legal protection given to the producers by the government authorities.

- The objective is to prevent the competitors from producing identical products.

- Monopoly due to legal rights, conferred by the government such as patent right, copy right, trade marks etc.

Question 5.

Monopoly and Monopolistic Competition.

Answer:

Monopoly:

- Monopoly is a market structure in which there is a single seller of a product which has no close substitute.

- There is no competition.

- There are strong barriers to entry.

- The demand for the product is less elastic as there are no close substitute.

- There is no selling cost incurred.

- Firm and industry are identical.

- Pure monopoly is an inelastic market.

Monopolistic Competition:

- It is a market structure in which large number of firms produce and sell products that are differentiated but close substitutes.

- There is competition among the firms producing very close substitutes.

- There is free entry and exit for the firms.

- Demand of the product is elastic as there are close substitutes for the product.

- Selling cost has an important role in Monopolistic Market.

- Under monopolistic competition firm and industry are not identical. They are a group.

- It is a realistic market.

Question 6.

Perfect Competition and Imperfect Competition.

Answer:

Perfect Competition:

- Perfect competition is a type of market where there are large number of firms producing homogeneous product.

- Each seller is price taker.

- Each individual firm controls only a small portion of the total supply.

- Each seller and buyer has perfect knowledge about the market situation.

- There are no types in perfect competitive market.

Imperfect Competition:

- Imperfect competition is a type of market where the product produced by the sellers may be similar or differentiated.

- Each seller is price maker.

- Each seller may control more or less portion of the total supply.

- Each seller and buyer may not have perfect knowledge about the market situation.

- Examples of imperfect market are monopoly, oligopoly, monopolistic competition, etc.

Question 7.

Local Market and National Market.

Answer:

Local Market:

- Local market is one in which goods are produced and sold mostly in local areas.

- Generally, perishable goods like milk, vegetables and bulky goods like sand have local market.

- Demand is limited in local market.

- Less variety is available in this market.

National Market:

- National Market is a domestic market in which goods are produced and sold within the country.

- Generally goods demanded by common man like wheat, rice, soaps have national market.

- Demand is very high in national market.

- Huge variety is available in this market.

Question 8.

Short Period and Long Period.

Answer:

Short Period:

- A short period is one during which the stock of a commodity can be changed to some extent.

- This is done by changing the quantity of variable factors like labour and raw material.

- Supply can be slightly adjusted to the change in demand.

- Demand plays more important role in determining the price.

- This period is usually upto 8-10 months.

Long Period:

- A long period is one during which the stock of a commodity can be fully changed.

- This is done by changing the size of the plant because all factors are variable.

- Supply can be fully adjusted to the change in demand.

- Supply plays more important role in determining the price.

- This period is usually form 1 year to 4-5 years.

3. Answer the following questions;

Question 1.

Define market.

Answer:

In economics, ‘Market’ refers to an arrangement through which buyers and sellers come in close contact with each other directly or indirectly for exchange of goods at a particular price. Thus, market is a network of dealings between buyers and sellers.

According to Augustin Cournot, “Economist understand by the term market, not any particular market place in which things are bought and sold, but the whole of any region in which buyers and sellers are in such close contact with one another that prices of the same goods tend to equality, easily and quickly.”

Thus, market is said to exist when –

- there are many buyers and sellers.

- they may be spread either to a place, region, country or world.

- goods are bought and sold at a price.

- people have the knowledge about market price.

- there is freedom of entry and exit of firms.

Question 2.

Classify the market on basis of place and explain.

Answer:

On the basis of place, market can be classified as follows :

1. Local Market : When the goods are produced and sold in the local area mainly due to the high transport cost are called local markets. For example bricks, stone, etc. Also perishable goods like fish, milk, etc. have local market.

2. National Market : Market confined to a domestic market in a country is called national market. E.g. cars, scooters, TV sets. These goods can be easily transported within the country.

3. International Market : Goods which can be sold in any part of the world have international market. E.g. Tea, cotton, petroleum. Such goods can be exported and imported at a low transport cost.

Question 3.

Classify the market on the basis of time and explain.

Answer:

On the basis of time market can be classified into following four types :

1. Very short period market: A very short period market is one during which supply of a commodity is fixed as it is already produced. This market is for a few days or maximum a week. So the price of the product is determined by demand. Eg. During festival time supply of fruits can be increased, so price rises.

2. Short period market : A short period market is said be a market upto one year. In this market supply of goods can be increased by increasing the variable factors like labour and raw material with the given fixed factors like machinery.

3. Long period market : A long period market is a market upto five years. In this J supply of a commodity can fully increased on demand as all factors of production can j be changed.

4. Very long period market : A very long period market is for more than five years. In this period there can be full adjustment of supply to demand.

Question 4.

Classify the market on the basis of competition and explain.

On the basis of competition, market can be { classified into two main types :

1. Perfect competition

2. Imperfect competition : It is further classified into.

(A) Monopoly

(B) Oligopoly

(C) Monopolistic Competition

According to Mrs. Joan Robinson, “Perfect competition prevails when the demand for the output of each producer is perfectly elastic. ” Hence, it is a market where there are large number of buyers and sellers engaged in buying and selling a homogeneous product at a single price in the market.

Imperfect competition:

(A) Monopoly: According to E. H. Chamberlin, “A monopoly refers to a single firm which has control over the supply of a product which has no close substitutes.” Hence, he can charge different prices from different buyers on the basis of demand.

(B) Oligopoly : An oligopoly is a market situation in which there are few sellers and a large number of buyers. Sellers may sell similar or different products which are close substitutes of each other.

(C) Monopolistic Competition : According to E. H. Chamberlin, “Monopolistic competition refers to competition among a large number of sellers producing close but not perfect substitutes.” Hence, this is a market which has features of both monopoly and perfect competition. E.g. for soaps, washing powders, etc.

Question 5.

What are the main features of Monopoly?

Answer:

Features of Monopoly:

1. Single Seller and Many Buyers : In

Monopoly market, there is only one seller or producer and many buyers. Monopoly firm does not have a rival in the market. So there is no competition.

2. No Close Substitute : The commodity produced by the monopolist does not have close substitutes. Hence they do not face any competition.

3. Entry Barriers : The fact that there is only one firm under monopoly means that other firms are restricted from entering the market. The entry barriers may be natural, legal or financial in nature.

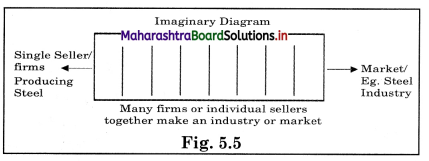

4. Firm Coincides with Industry : In monopoly market, the firm and industry are one and the same. In other words, there is no distinction between firm and industry.

5. Price Maker : In monopoly the seller is a Trice Maker’. Since the monopolist has control over the supply he can determine the price of his product.

6. Profit Maximisation (super normal profit) : A monopolist earns super normal profit. His decision regarding the price and the level of output are guided by profit maximisation motive.

7. Control Over Supply : The monopolisthas a complete hold over market supply as he is the sole producer.

Price discrimination : This implies charging different prices for the same l product to different buyers.

Question 6.

What are the different types of monopoly?

Answer:

There are different types of monopoly as analysed below:

1. Natural Monopoly : A natural monopoly arises when a particular type of natural resource is located in a particular region like petrol or crude oil in Gulf countries. Also natural advantages such as good location, business reputation, age – old establishment s etc., confer natural monopoly. Similarly, many professional skills, natural talents give monopoly power. E.g. A singer or actor has monopoly of his skill, talent.

2. Legal Monopoly : Legal monopolies are those monopolies which are recognised by law. Legal protection granted by the Government in the form of trade mark, copy rights, license etc., give monopoly power to the firms. Here the potential competitors are not allowed to copy the product registered under the given brand names, patents or trade marks according to the law.

3. Joint Monopoly or Voluntary

Monopoly : This monopoly arises through mutual agreement and business combinations like the formation of cartels, syndicate, trust etc. For e.g. Oil producing nations have come together and formed a Cartel OPEC (Organisation of Petroleum Exporting Countries).

4. Simple Monopoly : A simple monopoly firm charges a uniform price for its product to all the buyers.

5. Discriminating Monopoly : A discriminating monopoly firm charges different prices for the same product to different buyers. E.g. a doctor, a teacher, a lawyer, etc., charges different fees from the people. The practice of charging different prices from different buyers is called “Price discrimination.”

6. Private Monopoly : When an individual or a private firm enjoys the monopoly of manufacturing and supplying a particular product, it is called private monopoly. The main aim of private monopolist is profit maximisation.

7. Public Monopoly : When a field of production is solely owned, controlled and operated by the government, it is regarded as public monopoly. Eg. Public utility service like Railways, Electricity, Water Supply etc. Since these monopolies are service motivated and welfare oriented they are also called welfare monopolies.

Question 7.

What are the features of Oligopoly?

Answer:

The term Oligopoly is derived from the Greek words ‘Oligo’ which means few and ‘Poly’ which means sellers. Hence, following are its features –

1. Many buyers and few sellers : There are many buyers and a few sellers or firms (may be five or six) who dominate the market and have major control over the price of a product.

2. Interdependence : Since the number of firms are less, any change in price, output, product etc. by one firm will affect the rival firms and will force them to change their price, output, etc. E.g. In case of Coke and Pepsi in soft drink market.

3. Selling cost or advertising : Each firm in order to sell more of its product takes aggressive steps to advertise or through free samples. This helps them to capture larger sales.

4. Barrier to entry : The firm can easily exit from the industry whenever it wants, but to enter a new industry it has certain entry barriers like government license, patent right, etc.

5. Uncertainty : There is a great uncertainty in this market if the rival firms join hands and may try to fight each other.

6. Lack of Uniformity : The firms may produce either homogeneous or differentiated products. Eg. In automobile industry, Maruti, Indica are examples of differentiated product but cooking gas of Bharat Petroleum and Hindustan Petroleum are examples of homogeneous product or pure oligopoly.

4. State with reasons whether you agree or disagree with the following statements:

Question 1.

Single price prevails in perfect competition.

Answer:

Yes, I agree with this statement.

Single price prevails under perfect competition because.

- In perfect competition there are large number of buyers and sellers. A single seller nor a single buyer can influence the supply nor the demand and the price.

- In perfect competitive market price is determined by the interaction of the forces of demand and supply.

- Hence sellers and buyers are ‘Price takers’ only.

- Products sold in perfectly competitive market are homogeneous, and hence uniform or single price rules throughout the market for that product and also there is no selling cost incurred.

- There is perfect knowledge on the part of buyers and sellers about market conditions, which prevents price – discrimination, so single price prevails.

- Transport costs are ignored under perfect competition. If transport costs are involved then the prices of homogeneous goods would tend to differ.

Question 2.

Price discrimination is possible under monopoly.

Answer:

Yes, I agree with this statement.

Price discrimination is possible under Monopoly because :

- Monopoly is a market situation where there is only one seller who has complete control over the supply of commodity.

- So he is the price maker and also there is no close substitute for his product.

- Therefore, the buyer has no alternative but to buy the product from the monopolist or go without it.

- So a monopolist can charge different prices from different buyers for the same product.

- Generally he charges higher price from rich and lower price frpm poor.

- E.g. a doctor in a village may charge less fees from poor and high fees from rich.

Question 3.

Selling cost is incurred by a firm in Monopolistic Competition.

OR

In Monopolistic market, the selling cost is must.

Answer:

Yes, I agree with this statement.

Selling cost is incurred by a firm in Monopolistic Competition because –

- Monopolistic competition is a market where there are many sellers selling differentiated products which are substitutes for each other.

- So there is an element of ‘Monopoly’ and ‘Competition.’

- There is keen competition among group of monopolists producing same, though not identical product. So selling costs are incurred to increase the demand for the product.

- Selling costs are those costs which are incurred by the firms to create demand and increase the demand for its product through advertisements, publicity, salesmanship, etc.

- The main purpose of selling cost is to push up the sales of the product.

- The buyers in this market buy the product not by chance but by choice and preference. The advertisements, salesmanship etc can change the preference of the consumer towards their product.

Question 4.

A monopolist cannot control the supply of goods.

OR

Monopolist is price maker.

Answer:

No, I do not agree with this statement. A monopolist can control the supply of goods because –

- Monopoly is a market situation in which there is a single producer or seller of a product, which has no substitute.

- It means the entire production and supply of a particular product is in the hands of a single firm. Thus monopoly firm does not have a rival in the market. So he controls the supply.

- There is no distinction between a firm and an industry under monopoly.

- He is a price maker and normally fixes a higher price for profit maximisation.

Question 5.

Sellers and buyers are the price takers j in Perfect Competition.

Answer:

Yes, I agree with this statement.

- In perfect competition, there are large number of sellers.

- Individual seller contributes only a fraction of the total market supply.

- Similarly, there are large number of buyers.

- The individual buyers contribute only a fraction of the total market demand.

- Thus, a single seller or single buyer cannot influence the market price.

- The market price is determined by an interaction of market demand and market supply, which has to be accepted by the buyers and sellers.

- Therefore, a large number of sellers and buyers in a perfect competition are the price – takers.

Question 6.

The existence of Perfect Competition is an unrealistic concept. (Oct.’05)

Answer:

Yes, I agree with this statement.

- Perfect competition is based on certain fundamental assumptions, which are hard to realise because such ideal conditions are not found in real life.

- In real economic world, products are not homogeneous. Products are differentiated due to influence of advertisement, difference in quality, design, packing etc.

- Due to ignorance the buyers and sellers do not possess perfect knowledge of market conditions.

- This leads to imperfect competition and discriminatory price for identical product.

- Customs and sentiments, also curtail the freedom of buyers and sellers.

- Also due to social and moral constraints factors of production particularly labour is imperfectly mobile.

- For all these reasons perfect competition is a myth. It is an unrealistic market.

Question 7.

Monopolistic Competition is not found in real life.

OR

Monopolistic Competition does not enjoys practical existence. (Mar., ’09)

Answer:

No, I do not agree with this statement.

OR In reality, there is monopolistic competition.

Answer:

Yes, I agree with this statement.

- In real world we find a market in which the characteristics of both Monopoly and Competition are interwoven.

- For instance we find in the market many producers producing same product ‘Soap’ but it is not homogeneous.

- The soap for example produced by Hindustan Lever and ITC and Proctor & Gamble is slightly different in shape, size, fragrance etc., like Lux is different from Dove and Vivel.

- Each producer is the monopolist in a way of his own brand value but has to face competition from his rival.

- All these producers compete with each other in selling soaps.

- Thus monopolistic competition is found in real life.

Question 8.

A seller is a price maker in monopoly.

Answer:

Yes, I agree with this statement.

- In monopoly market there is a single seller of a product. The aim of the monopolist is to earn maximum profit.

- Being a single seller, the monopolist has complete control over the market supply.

- The monopolist can thus have control over the price. He is, thus, a price maker.

Question 9.

Public Monopoly is welfare oriented.

Answer:

Yes, I agree with this statement.

- Public Monopoly is solely owned, operated and controlled by the Government.

- Government owned firm provide utility service. It does not aim at profit but welfare maximisation.

- Utility services like the Railways, banks, water supply etc., if left to the private firms will lead to exploitation.

- This is because such services have inelastic demand, so if it is left to private firm they will charge high prices.

Question 10.

Perishable goods have local market.

Answer:

Yes, I agree with this statement.

Perishable goods have local market because:

- Market confined to a particular area or locality like a village or town is called local market.

- Perishable goods are those goods which last for 2-3 days e.g. Goods like fish, milk, fruits, vegetables, flowers, etc. usually have local market.

- Since, such goods are get destroyed soon and if transported to far off markets places, transport cost would also be high, increasing the cost of goods.

Hence, perishable goods usually have local market.

Question 11.

Market in Economic is a place where goods are bought and sold.

Answre:

No, I do not agree with this statement.

- In common language, the term market is generally understood as a place buyers and sellers meet to buy and sell the commodities.

- For market to exist, there should be arrangement through which buyers and sellers come in close contact with each other directly or indirectly for exchange of goods and services.

- This exchange may be by way of telephone, tele-marketing, internet all over the world.

5. Answer in detail:

Question 1.

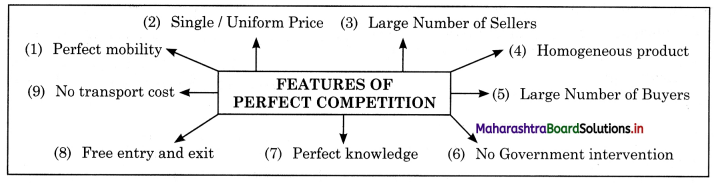

What are the features / characteristics / conditions / assumptions / peculiarities of perfect competition?

Answer:

(1) Perfect Mobility of Factors of Production : Factors of production that is land, labour, capital are perfectly free to move from one firm to another or from one industry to another from one region to another or from one occupation to another. This ensures freedom of entry and exit for individuals and firms.

(2) Single / Uniform Price : There exists a single price for homogeneous product in the entire market at a given point of time. The price is determined by forces of demand and supply.

(3) Large Numbers of ellers : There are many sellers in this market. The number of sellers (firms) are so large that a single seller cannot influence the market price nor the total output in the market (Industry). The contribution of one seller is insignificant and microscopic. The price in the market is determined by the forces of market demand and market supply. Hence, a firm or seller is a ‘price taker’ and not a ‘price maker.’

(4) Homogeneous Product : The products produced by all the firms in the industry are identical and are perfect substitute to each other. The products are identical in shape, size, colour, etc. and hence uniform price rules the market for the product.

(5) Large Number of Buyers : There are large number of buyers in the market. One individual buyer’s demand is only a small fraction of total market demand so he is not in a position to influence the price. He is a price taker.

(6) No Government Intervention : It is assumed that the government does not interfere with the working of market economy. There are no tariffs, subsidies, licensing policy or other government interventions. This non – intervention of government is necessary to permit free entry of firms and automatic adjustment of demand and supply. In short, laissez faire policy prevails under perfect

(7) Perfect Knowledge : There is perfect knowledge on the part of buyers and sellers regarding the market conditions especially regarding market price. As a result no buyer will pay a higher price than the market price and no seller will charge a lower price than the market price. So a single price would prevail for a commodity in the entire market.

(8) Free Entry and Free Exit : There is freedom for new firms or sellers to enter the industry or market. There are no legal, j economic or any other type of restrictions or; barriers for new firms to enter the industry or an existing firms to quit the industry, Entry of new firm usually takes place j when existing firms enjoy abnormal profit. Similarly, existing firms quit the industry when they face losses.

(9) No Transport Cost: It is assumed that all firms are close to the market and hence there is no transport cost. If the transport cost are added to the price of product then the homogeneous commodity will have different prices depending upon the distance from the place of supply to the market

Question 2.

How is the equilibrium price determined under perfect competition?

Answre:

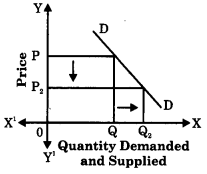

Under perfect competition price is determined by the two forces of Demand and Supply. The interaction of demand and supply determines the equilibrium price of a commodity in the market. Equilibrium price is that price at which quantity demanded is equal to the quantity supplied. According to Marshall, demand and supply are like two blades of a pair of scissors. Just as the cutting of cloth is not possible without the use of both the blades, the equilibrium price of a commodity cannot be determined either by the force of demand or supply alone. Both together determine the price. This can be explained with the help of a table and a graph.

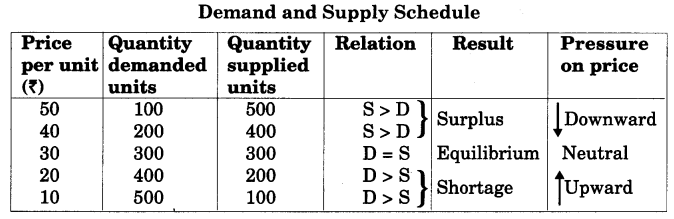

From the above table, we see that at price of ₹50 and ₹40 per unit, the supply is more than demand. This is because more sellers want to supply at higher prices due to greater profit margin but buyer’s demand is less at a higher price, so there is excess supply (i.e. S >D). Here the number of sellers are more than buyers, the competition among sellers will put a downward pressure on price. The price will fall to ₹30 as a result supply will contract and demand will expand. Now at ?30, the demand becomes equal to supply (D = S). So ₹30 is called the equilibrium price.

Now suppose the market price is ₹10, or ₹20 per unit, which is less than the equilibrium price, the demand is greater i.e. 500 and 400 units than supply which is 100 and 200 units (D > S). There is excess of demand because buyers want to buy more at a lower price but sellers want to sell less as the profit margin is less. Hence there will be shortage of supply. Now, since the buyers are more the competition among buyers will put a upward pressure on the price, so the price rises to ₹30.

Here, some of the sellers will exit the market due to the high cost of production and low market price, which lowers the profit margin. But there will be entry of new buyers with low marginal utility. So demand rises and becomes equal to supply. ₹30 will prevail in the market as long as demand and supply conditions remain the same. It is a stable price where quantity demanded and supplied is 300 units.

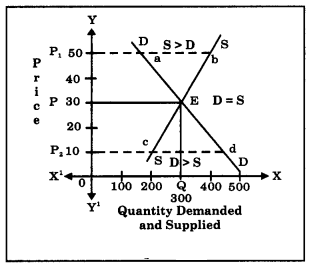

When the above demand and supply) schedule is represented graphically, we get S demand curve DD sloping downward and supply curve SS sloping upward.

The demand curve DD intersects the; supply curve SS at point E at which the c equilibrium price determined is OP and OQ is equilibrium quantity demanded and supplied.

If the price is OP1 which is higher than the equilibrium price OP there is excess s supply i.e. ab. This will force the prices to ( fall downward from seller side. If the price ) falls to OP2 below the equilibrium price OP there is excess demand i.e. cd. This willforce the price to rise upward. In this way the equilibrium price OP is determined by forces of demand and supply. At equilibrium price quantity demanded is equal to quantity supplied i.e. OQ.

Question 3.

What are features of monopolistic competition?

Answer:

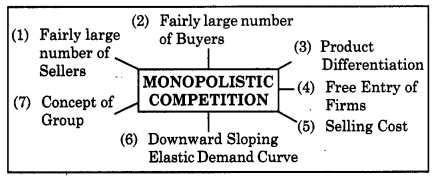

Features of Monopolistic Competition

(1) Fairly large number of Sellers : There are large number of sellers selling closely related, but not identical products. There is tough competition among sellers. An individual seller supply is just a small part of the total supply, so he has limited degree l of control over market supply and price. Each firm (seller) can formulate its own price and output policy independently.

(2) Fairly large number of Buyers: There are large numbers of buyers in a monopolistic competition market. Each buyer enjoys his preference over a particular brand and chooses to buy a specific brand of product. Hence, the buying is by choice and not by chance.

(3) Product Differentiation : The most distinguishing feature of monopolistic competition is that the product produced by different firms are not identical, they are slightly different from each other but they are close substitutes. The product differentiation can be done in different ways like may be in the form of brand names say Raymonds. It can be differentiated in terms of colour, size, design, etc., say soap, mobiles etc., or through sales technique. For e.g. cars, two wheelers, air conditioners, etc.

(4) Free Entry of Firms: A firm is free to enter the market as there are no entry barriers. Similarly there are no restrictions if the firm wants to quit the market. Freedom of entry leads to occurrence of only normal profit in the long run.

(5) Selling Cost : One of the special features of monopolistic competition is the selling cost. Selling costs are those costs, which are incurred by firms to create more and more demand for its products through advertisement, salesmanship, free samples, exhibitions, etc.

(6) Downward Sloping Elastic Demand Curve : The demand curve faced by each firm is downward sloping and comparatively more elastic. It implies that an individual firm can sell more only by reducing the price.

(7) Concept of Group : Under monopolistic competition, Prof. E. H. Chamberlin introduced the concept of group in place of Marshallian concept of industry. Industry means a number of firms producing identical products. A group means a number of firms producing differentiated product, which are close substitutes.

Question 4.

What is monopoly? Explain the features of monopoly.

Answer:

Monopoly: According to E. H. Chamberlin, “A monopoly refers to a single firm which has control over the supply of a product which has no close substitutes.” Hence, he can charge different prices from different buyers on the basis of demand.

Features of Monopoly:

1. Single Seller and Many Buyers : In

Monopoly market, there is only one seller or producer and many buyers. Monopoly firm does not have a rival in the market. So there is no competition.

2. No Close Substitute : The commodity produced by the monopolist does not have close substitutes. Hence they do not face any competition.

3. Entry Barriers : The fact that there is only one firm under monopoly means that other firms are restricted from entering the market. The entry barriers may be natural, legal or financial in nature.

4. Firm Coincides with Industry : In monopoly market, the firm and industry are one and the same. In other words, there is no distinction between firm and industry.

5. Price Maker : In monopoly the seller is a Trice Maker’. Since the monopolist has control over the supply he can determine the price of his product.

6. Profit Maximisation (super normal profit) : A monopolist earns super normal profit. His decision regarding the price and the level of output are guided by profit maximisation motive.

7. Control Over Supply : The monopolisthas a complete hold over market supply as he is the sole producer.

Price discrimination : This implies charging different prices for the same l product to different buyers.

Question 5.

Define perfect competition and explain price determination under perfect competition.

Answer:

According to Mrs. Joan Robinson, “Perfect competition prevails when the demand for the output of each producer is perfectly elastic. ” Hence, it is a market where there are large number of buyers and sellers engaged in buying and selling a homogeneous product at a single price in the market.

Imperfect competition:

Under perfect competition price is determined by the two forces of Demand and Supply. The interaction of demand and supply determines the equilibrium price of a commodity in the market. Equilibrium price is that price at which quantity demanded is equal to the quantity supplied. According to Marshall, demand and supply are like two blades of a pair of scissors. Just as the cutting of cloth is not possible without the use of both the blades, the equilibrium price of a commodity cannot be determined either by the force of demand or supply alone. Both together determine the price. This can be explained with the help of a table and a graph.

From the above table, we see that at price of ₹50 and ₹40 per unit, the supply is more than demand. This is because more sellers want to supply at higher prices due to greater profit margin but buyer’s demand is less at a higher price, so there is excess supply (i.e. S >D). Here the number of sellers are more than buyers, the competition among sellers will put a downward pressure on price. The price will fall to ₹30 as a result supply will contract and demand will expand. Now at ?30, the demand becomes equal to supply (D = S). So ₹30 is called the equilibrium price.

Now suppose the market price is ₹10, or ₹20 per unit, which is less than the equilibrium price, the demand is greater i.e. 500 and 400 units than supply which is 100 and 200 units (D > S). There is excess of demand because buyers want to buy more at a lower price but sellers want to sell less as the profit margin is less. Hence there will be shortage of supply. Now, since the buyers are more the competition among buyers will put a upward pressure on the price, so the price rises to ₹30.

Here, some of the sellers will exit the market due to the high cost of production and low market price, which lowers the profit margin. But there will be entry of new buyers with low marginal utility. So demand rises and becomes equal to supply. ₹30 will prevail in the market as long as demand and supply conditions remain the same. It is a stable price where quantity demanded and supplied is 300 units.

When the above demand and supply) schedule is represented graphically, we get S demand curve DD sloping downward and supply curve SS sloping upward.

The demand curve DD intersects the; supply curve SS at point E at which the c equilibrium price determined is OP and OQ is equilibrium quantity demanded and supplied.

If the price is OP1 which is higher than the equilibrium price OP there is excess s supply i.e. ab. This will force the prices to ( fall downward from seller side. If the price ) falls to OP2 below the equilibrium price OP there is excess demand i.e. cd. This willforce the price to rise upward. In this way the equilibrium price OP is determined by forces of demand and supply. At equilibrium price quantity demanded is equal to quantity supplied i.e. OQ.