Balbharti Maharashtra State Board Class 12 Economics Important Questions Chapter 9 Money Market and Capital Market in India Important Questions and Answers.

Maharashtra State Board 12th Economics Important Questions Chapter 9 Money Market and Capital Market in India

1. A. Choose the correct option:

Question 1.

Money Market is a market for lending and borrowing of ………….. funds.

(a) long term

(b) medium-term

(c) short term

(d) all of these

Answer:

(c) short term

![]()

Question 2.

The financial system of the country is responsible for ………….. of funds.

(a) mobilization and allocation

(b) distribution of investment

(c) optimum resources

(d) all of these

Answer:

(a) mobilization and allocation

Question 3.

………….. is the only active money market centre in India.

(a) Nagpur

(b) Madras

(c) Mumbai

(d) Kolkata

Answer:

(c) Mumbai

Question 4.

Central Bank has the ………….. of cash reserve of commercial Bank in the country.

(a) monopsony

(b) monopoly

(c) oligopoly

(d) autopsony

Answer:

(b) monopoly

Question 5.

The Central Bank acts as a ………….. of cash reserve of Commercial Bank in the country,

(a) head

(b) leader

(c) custodian

(d) protector

Answer:

Question 6.

………….. is the apex body of the monetary and banking system of Commercial Banks in the country.

(a) Commercial Bank

(b) Central Bank

(c) Government

(d) Co-operative Bank

Answer:

(b) Central Bank

![]()

Question 7.

Bank rate is ………….. measure of credit control.

(a) quantitative

(b) qualitative

(c) selective

(d) effective

Answer:

(a) quantitative

Question 8.

Reserve Bank of India was established in …………..

(a) 1937

(b) 1936

(c) 1935

(d) 1934

Answer:

(c) 1935

Question 9.

The operation of direct buying and selling of securities by central bank in the money market is called …………..

(a) open market operation

(b) credit creation

(c) moral suasion

(d) closed market operation

Answer:

(a) open market operation

Question 10.

………….. account is opened by businessmen, corporate bodies, etc.

(a) Saving

(b) Current

(c) Fixed

(d) Recurring

Answer:

(b) Current

Question 11.

………….. is a primary function of commercial banks.

(a) Safe deposit vault

(b) Letter of credit

(c) Accepting deposits

(d) Transfer of funds

Answer:

(c) Accepting deposits

![]()

Question 12.

Every loan creates .

(a) deposits

(b) credit

(c) profit

(d) debit

Answer:

(a) deposits

Question 13.

Enactment of the Co-operative Credit Societies Act .

(a) 1903

(b) 1904

(c) 1905

(d) 1906

Answer:

(b) 1904

Question 14.

was the 1st Development Financial Institution to be established in 1948.

(a) IFCI

(b) IDBI

(c) ICICI

(d) HSCBI

Answer:

(a) IFCI

Question 15.

DFHI was set up on the recommendation of the committee.

(a) Narsimhan

(b) Vaghul

(c) Vaghale

(d) Tandon

Answer:

(b) Vaghul

Question 16.

The activities of unorganized money market are largely confined to the areas.

(a) city

(b) urban

(c) rural

(d) none of these

Answer:

(c) rural

Question 17.

important source of funds in unbanked areas which provide loans directly to agriculture, trade and industry.

(a) Indigenous bankers

(b) EXIM Bank

(c) IDBL

(d) HSCB Bank

Answer:

(a) Indigenous bankers

Question 18.

charge high rate of interest to the people.

(a) RBI

(b) Commercial Bank

(c) Money lenders

(d) LIC

Answer:

(c) Money lenders

Question 19.

………………. short term instruments issued by the RBI on behalf of the government to meet temporary liquidity shortfalls.

(a) Commercial papers

(b) Call money market

(c) Treasury Bills

(d) Commercial Bills

Answer:

(c) Treasury Bills

(B) Complete the Correlation

- RBI was set up : Hilton Young Commission :: DFHI was set up : ………………..

- Open market operation : ……………….. :: Moral suasion : Qualitative method

- Deposits that are repayable after a certain period of time : Time deposits :: Deposits that are withdrawable on demand : ………………..

- Commercial Banks : Credit creation :: ……………….. : Controller of credit

- SEBI : 1998 :: NSE : ………….

Answer:

- Vaghul committee

- Quantitative method

- Demand deposits

- RBI

- 1992

![]()

(C) Suggest the economic terms for the given statements.

(1) Account that are operated by salaried class and small traders.

(2) Accounts is opened by businessmen, corporation or trust.

(3) Source of funds in unbanked areas which provide loans directly to agriculture, trade and industry.

(4) It is unsecured negotiable instrument in bearer form issued by Commercial banks and Development Finance Institutions.

(5) It is also known as the gilt-edged market.

(6) Market deals with securities already issued by companies.

(7) It act as a link between the investors and the borrower to meet the financial objectives of both the parties.

(8) It deals with the shares and debentures issued by old and new companies.

(9) Market for long term funds.

(10) Fund to promote investors awareness.

Answer:

- Saving A/c

- Current A/c

- Indigenous bankers

- Certificates of deposits

- Government Securities

- Secondary Market

- Financial intermediaries

- Industrial Securities Market

- Capital Market

- IEPF

(D) Find the odd word

(1) Financial Instruments :

Bonds, Demand, Equity Shares, Derivatives.

Answer:

Demand

(2) Unorganised Sector :

Indigenous Bankers, Money lenders, Unregulated Non-Bank Financial Intermediaries, Co-operative Banks.

Answer:

Co-operative Banks

(3) Functions of RBI:

Collection and Publication of Data, Controller of Credit, Credit Creation, Bankers Bank.

Answer:

Credit Creation

(4) Functions of Commercial Bank :

Acceptance of Deposits, Lending loans and advances, Credit Creation, Banker’s Bank.

Answer:

Banker’s Bank

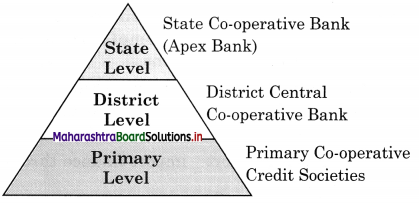

(5) Co-operative Credit Structure : State level, District level, Secondary level, Primary level

Answer:

Secondary Level

(6) Money Market Instruments :

Treasury Bills, Certificate of Deposits, Commercial Bills, Discount and Finance House of India.

Answer:

Discount and Finance House of India

(E) Complete the following statements.

(1) Method of withdrawing money without going to the bank is by

Answer:

ATM

(2) The Account in which certain amount of money is deposited every month regularly for a fixed duration is .

Answer:

Recurring A/c

(3) Credit creation is an important function of Bank.

Answer:

Commercial

(4) Saving Bank Account is suitable for people

Answer:

salaried

(5) Higher rate of interest is paid on deposits.

Answer:

Fixed

(6) Currency rate of India to other currency means

Answer:

exchange rate

![]()

(7) system economies the use of cash.

Answer:

Clearing House

(8) The works as friend, philosopher and guide to Commercial Bank.

Answer:

Central Bank

(9) Bank grants loans to government.

Answer:

Central

(10) When money is borrowed or lent for a day, it is known as

Answer:

Call / Notice money

(11) A well-developed money market ensures successful implementation of the policy.

Answer:

monetary

(F) Choose the wrong pair :

I.

| Group ‘A’ | Group ‘B’ |

| 1. Central Bank | Apex Banking Institution |

| 2. Clearing House system | Specialised institution for agriculture |

| 3. Credit Control | Quantitative measure |

| 4. Money Market | Short term fund |

Answer:

Wrong pair : Clearing House system Specialised institution for agriculture

II.

| Group ‘A’ | Group ‘B’ |

| 1. Commercial Bank | Acceptance of Deposit |

| 2. IFCI | 1948 |

| 3. Co-operative Credit Society Act | 1904 |

| 4 Discount and Finance House of India | 1980 |

Answer:

Wrong pair : Discount and Finance House of India – 1980

(G) Assertion and Reasoning.

Question 1.

Assertion (A) : Illegal practices have also affected the smooth functioning of capital market. :

Reasoning (R) : Price manipulation or ( price rigging on the other hand means to simply raise the prices of shares through ) buying and selling of shares within certain individual themselves for personal gains. ;

(i) (A) is true, but (R) is false

(ii) (A) is false but (R) is true

(iii) Both (A) and (R) are true and (R) is the correct explanation of (A)

(iv) Both (A) and (R) are true and (R) is not the correct explanation of (A)

Answer:

(iv) Both (A) and (R) are true and (R) is the correct explanation

(H) Choose the correct pair :

I.

| Group ‘A’ | Group ‘B’ |

| Demat Account | (a) Commercial Bank |

| Overdraft | (b)Ancillary function |

| Credit creation | (c) 1949 |

| Banking Regulation Act | (d) 1935 |

| (e) Amount withdrawn above the actual balance |

Ans.

(1)-(b), (2)-(e), (3)-(a), (4) – (c)

II.

| Group ‘A’ | Group ‘B’ |

| Local area Banks | (a) RBI |

| Liquidity Adjustment Facility (LAF) | (b) Primary and Secondary markets |

| Industrial Securities market | (c) Money Market |

| Stock Exchange | (d) Capital Market |

| (e) August, 1996 |

Answer:

(1)-(e), (2)-(a), (3)-(b), (4) – (d)

Q.2.[A] Identify and explain the concept from given illustrations.

Question 1.

Santosh invested money in share market and the broker does fraud in company.

Answer:

Concept: Financial Scams

Explanation : Financial scams are the frauds and manipulations done by the stock brokers for their personal benefits. Increasing number of financial frauds have resulted in irreparable loss for the capital market.

It also leads to public distrust and loss of confidence among the individual investors.

Question 2.

XYZ Bank Provides cash credit, overdraft facility and loan to its customer.

Answer:

Concept: Providing loans and advances by Commercial Bank

Explanation : Commercial Bank mobilize savings and lend these funds to institutions and individuals for various purposes.

Based on tenures, loans include call loans, short term, medium term and long term loans.

Longer the duration of the loans, greater will be the rate of interest.

Beside this bank also provide cash credit, overdraft facility as well as discounting of bills of exchange.

![]()

(B) Distinguish between:

Question 1.

Central Bank and Commercial Bank.

Answer:

Central Bank:

- The central bank is the apex banking institution whose main function is to control, regulate and stabilise the monetary system of the country in the national interest.

- The main function of central bank is to control, regulate and stabilise the banking and monetary system of the country.

- It does not deal with public directly. It acts as the banker to government and bankers bank.

- It enjoys the monopoly right to print and issue currency notes.

- Central Bank controls the credit.

- There is only one Central Bank in India. R.B.I. is owned by Government.

Commercial Bank:

- A commercial bank is abusiness organisation which basically accepts deposits from public and lends to others who need fund and create credit.

- The main function commercial bank is to accept deposits and lend loans and advances.

- It deals with the public directly. They are banker to general public.

- Commercial banks do not possess such rights.

- Commercial banks create credit.

- Owned by private or government. There are several commercial banks like State Bank of India, ICICI Bank, Canara Bank, etc.

Question 2.

Quantitative Credit Control and Qualitative Credit Control. (Mar. ’18)

Answer:

Quantitative Credit Control:

- This method aims at controlling credit by expanding or contracting the volume of credit in the banking system.

- The important quantitative measures to control credit are

(1) Bank Rate

(2) Open Market Operation

(3) Varying Cash Reserve ratio. - During inflation quantitative measures adopt the strategy of contracting the volume of credit so as to reduce money supply. During inflation such methods are applied to encourage expansion of credit and expand money supply.

- They are macro economic in nature and influence the whole economy.

Qualitative Credit Control:

- It aims at controlling credit by checking the purpose or use of the credit.

- Selective control measures include the following:

(1) Changing the market.

(2) Regulation of consumer credit

(3) Issue of directives

(4) Rationing of credit

(5) Moral suasion. - The main strategy of selective credit control measures is to ensure that credit money does not reach undesirable and non – productive channels.

- They are micro in nature and do not influence the whole economy.

Question 3.

Current Account and Saving Account.

Answer:

Current Account:

- This account is usually opened by businessmen, industrial enterprises, public bodies, etc.

- This account facilitates regular business transactions.

- There is no interest paid on current account.

- There is no restriction on withdrawals.

Saving Account:

- This account is held by the households, salaried class, small traders, etc.

- The main purpose of saving account is to encourage saving habits among people.

- The saving account earns a nominal rate of interest.

- Withdrawals are allowed subject to certain restrictions.

Question 4.

Fixed Deposits and Saving Deposits.

Answer:

Fixed Deposits:

- Fixed Deposits are time bound deposits, where money is deposited for a specific period of time.

- The main objective is to earn high interest and to get lumpsum amount on maturity.

- It cannot be withdrawn before maturity but one can close the account before maturity with loss of interest.

- The rate of interest is high. It can be 6% to 10% depending upon the period of deposit.

Saving Deposits:

- Saving deposits are a kind of demand deposits, which is held by households or individuals for the purpose of savings.

- Safety is the major objective of saving accounts.

- Withdrawals are allowed subject to certain restrictions.

- The saving account earns nominal rate of interest. At present it is about 4 to 4.5% per annum.

Question 5.

Current Deposits and Recurring Deposits.

Answer:

Current Deposits:

- It is a kind of demand deposit which is mostly held by companies, institutions, government and individual for the sake of business transactions.

- It is suitable for business firms for the purpose of transactions.

- There are no restrictions on withdrawals.

- There is no interest paid.

Recurring Deposits:

- These are deposits under which people pay a specified amount at a regular interval of time for a given period of time.

- It is suitable for the salaried, poor and lower middle class who can save a certain amount of money regularly every month.

- The amount can be withdrawn after a specific period of time.

- The interest rate is higher.

![]()

Question 6.

Current Deposits and Fixed Deposits,

Answer:

Current Deposits:

- It is a kind of demand deposit which is usually held by companies, institutions, government and individuals for the sake of business transactions.

- There are no restriction on withdrawals.

- No interest is paid to current account or deposits.

- The main purpose of current account is to facilitate regular transactions.

Fixed Deposits:

- Fixed deposits are a kind of time deposits which is deposited for a specific period.

- The amount deposited cannot be withdrawn before maturity period.

- The rate of interest paid is high.

- The main purpose is to get a lumpsum amount on the maturity of the deposit.

3. Answer the following questions :

Question 1.

Explain the reforms introduced in the capital market.

Answer:

Reforms introduced in the Capital Market are as follows :

- SEBI was established in 1988 and given statutory power in 1992 to protect interest of investors.

- NSE, the leading stock exchange in India was established in 1992.

- Introduction of Computerised Screen Based Trading System (SBTS).

- Introduction of Demat A/c in 1996 to facilitate easy purchase and sale of securities.

- Increased access to global funds, Indian companies was permitted through ADRs and GDRs.

- Investors Education and Protection Fund (IEPF) was created in 2001 to promote awareness among investors and protecting the interest of the investors.

Question 5.

What are the reforms introduced in the money market?

Answer:

Following are the reforms introduced in the Money Market:

- Introduction of New Money Market Instruments : In order to widen and diversify the Indian money market, RBI has introduced many new money market instruments such as 182 Days treasury bills, 364 day treasury bills, CDs and CPs. Through these instruments, the government, commercial banks, financial institutions and corporates can raise funds through the money market.

- Liquidity Adjustment Facility (LAF) : RBI has introduced LAF for adjusting liquidity through repos and reverse repos to stabilise the short-term interest rates or call rates.

- Deregulation of Interest Rates : Ceiling on interest rates on the call money and inter bank short term deposits was removed and the rates were permitted to be determined by the market forces.

- National Electronic Fund Transfer (NEFT) and Real Time Gross Settlement (RTGS) were introduced as an improved payment infrastructure.

- Electronic dealing system was introduced.

4. State with reasons whether you : agree or disagree with the following statements :

Question 1.

There is four tier co-operative credit l bank structure in India.

Answer:

No, I do not agree with this statement.

There are three tier of credit co- operative bank structure i.e. at –

Primary Level – Primary Co operative Credit Societies.

District Level – District Central Co operative Banks.

State Level – State Co operative Banks.

Question 2.

Moneymarket consist only unorganised sector in India.

Answer:

No, I do not agree with this statement.

Money market consist organized as well as unorganized sector in India

The organized sector of money market consist of the RBI, Commercial Banks Co-operative Banks, Development Financial Institutions (DFIs) and Discount and Finance House of India (DFHI) and the unorganized sector of money market consist of Indigenous Bankers, Money lenders and Unregulated Non-Bank Financial Intermediaries.

Question 3.

Unit Trust of India was the first development financial institution in India.

Answer:

No, I do not agree with this statement.

Development Financial Institution are agencies that provide medium and long term financial assistance.

They help in the development of industry, agriculture and other key sectors.

In includes many financial institutions, like – ICICI, IDBI, IIBI and UTI.

IFCI was the first development financial institution established in 1948.

Question 4.

Compared to advanced countries, the Indian money market is less developed.

Answer:

Yes, I do agree with this statement.

Indian money market is relatively underdeveloped, when compared to advanced markets like London and New York money markets.

Its main weaknesses are explained as below:

Following are the problems of money market in India:

(a) Shortages of Funds : Generally, there is shortage of funds in Indian Money Market on account of various factors like inadequate banking facilities, low savings, lack of banking habits, existence of parallel economy,- etc. have also been responsible for the paucity of funds in the money market.

(b) Existence of Unorganised Money Market : This is one of the major defects of Indian Money Market. It does distinguish between short term and long term finance, and also between the purposes of finance. Since it is outside the control and supervision of RBI. It limits the RBI’s control over money market.

(c) Delays in technological up-gradation: Use of advanced technology is a pre requisite for the development and smooth functioning of financial markets. Delays in up-gradation of technology hampers the working of the money market.

(d) Absence of Well Organized Banking Sector : Branch expansion was very slow before bank nationalization in 1969. Even now the banks are largely concentrated in large towns and small cities. There is lack of movement of funds. Indian banking system is not yet a well organized sector.

(e) No Uniformity in the rates of interest:

There exists too many rates of interest in the Indian Money Market such as the borrowing rate of government, deposits and lending rates of co-operatives and commercial banks, lending rates of financial institutions, etc. This is due to lack of mobility of funds from one section of the money market to another.

![]()

5. Answer in detail:

Question 1.

Explain the role of money market in India ?

Answer:

(A) Meaning:

Money market is a market for lending and borrowing short term funds.

It is a market for near money.

It deals in short term instruments like trade bills, government securities, promissory notes, etc.

Money market centres are located at Mumbai, Delhi and Kolkata. Money market consists of organised as well as unorganised sector.

Role of Money Market in India :

1. Portfolio Management : Money market deals with different types of financial instruments which are designed to suit the ( risk and return preferences of the investors. This enables the investors to hold a portfolio of different financial assets which in turn, helps in minimizing risk and maximizing returns.

2. Implementation of monetary policy :

Various monetary policies are implemented by the Central Bank, with an aim to manage the quantity of money, to meet the requirements of different sectors of the economy and to increase the pace of economic growth. Money market ensures successful implementation of these monetary policies. It also guides the central bank in developing an appropriate interest policy.

3. Growth of Commerce, Industry and Trade : Money market facilitates discounting bills of exchange to local and international traders who are in urgent need of short-term funds. It also provides working capital for agriculture and small scale industries.

4. Financial requirements of the Government : Money market helps the Government to fulfil its short term financial requirements on the basis of Treasury Bills.

5. Economizes the use of cash : Money market deals with various financial instruments that are close substitutes of money and not actual money. Thus, it economizes the use of cash.

6. Equilibrating mechanism : Money market helps to establish equilibrium between the demand for and supply of short term funds by allocating rationally the available resources and thus mobilizing the savings of public into fruitful investment channels.

7. Liquidity Management : Money Market, through the monetary authorities facilitates better management of liquidity and money in the economy. This, in turn, leads to economic stability and development of the country.

8. Short-term requirements of borrowers :

Money market provides short-term financial needs of the borrowers at reasonable prices.

Question 4.

Write note on Recent Developments in banking sector.

Answer:

Recent developments in banking sector :

(a) Small Finance Banks : The main aim of small finance banks is to promote financial assistance to small business units, small and marginal farmers, micro and small industries and other unorganised sectors of the economy.

It also assists with high technology at low cost of operations.

(b) Payments Banks : Payment banks are like other banks only, but they operate on a smaller scale without involving any credit risk.

It can carry almost all banking operations but cannot advance loans or issue credit cards.

It can accept deposits upto ₹ one lakh.

It can offer following services to its customers – remittance services, mobile payments, ATM facility, Debit cards, net banking, etc.

(c) Universal Banks : Universal banks refer to those banks that offer a wide range of financial services like commercial banking and investment banking and also offer other services, especially insurance service. It is a multipurpose and multi-functional financial supermarket providing both banking and financial services through a single window.

(d) Local Area Banks : Local area bank scheme was introduced in August, 1996. It was established to mobilize rural savings by private local banks and make them available for investments in the local areas. This helps to bridge the gap in credit availability and strengthens the institutional credit system in the rural and semi-urban areas.